Global "double dip" on track

Simon Ward

Simon Ward

3 Comments

3 Comments

A “double dip” in the global economy suggested by monetary trends appears to be playing out, with weakness likely to intensify into late 2023.

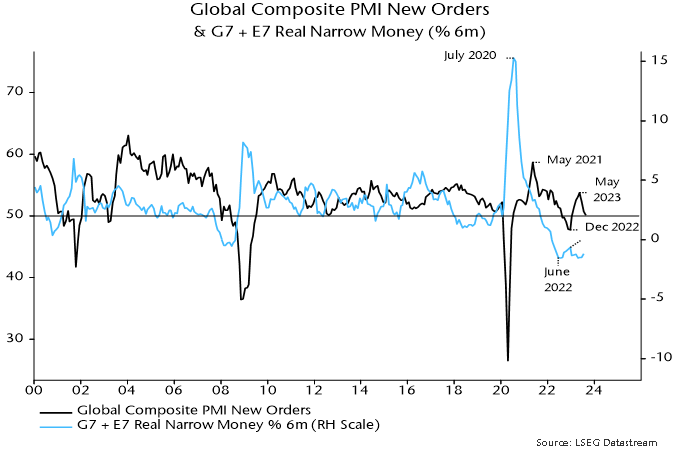

The global composite PMI new orders index – a timely coincident indicator – continued its decline from a May peak last month. A relapse had been suggested by a fall in six-month real narrow money momentum from December 2022 – see chart 1.

Chart 1

The year-to-date low in real money momentum occurred in April but there was little recovery through July and another decline is possible. The suggestion is that the PMI will fall further into Q4 and remain weak into early 2024.

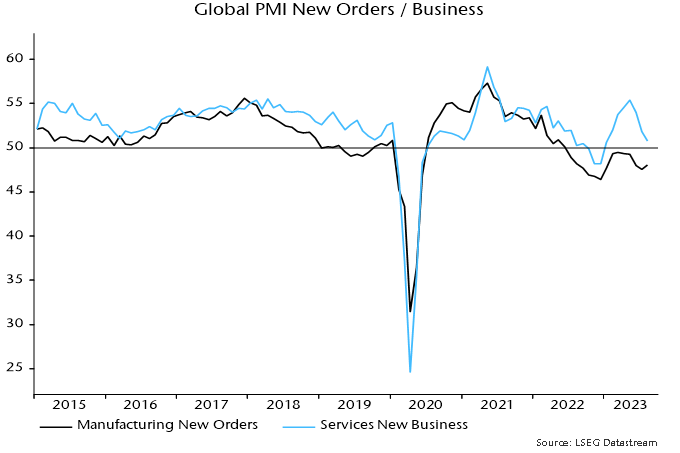

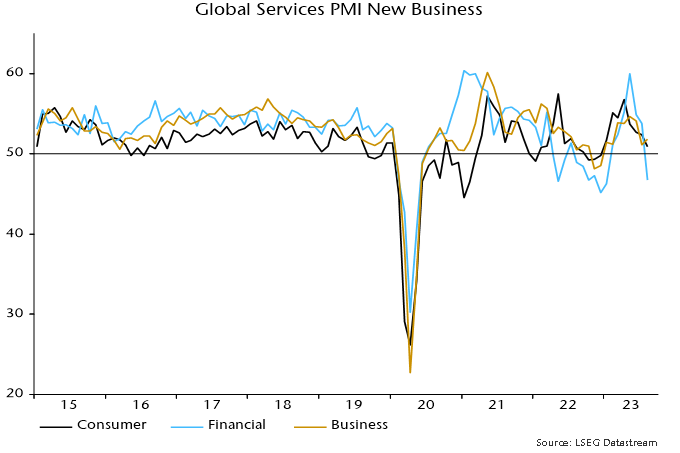

As expected, the composite PMI fall is being driven by services converging down towards weak manufacturing – chart 2. The August decline in services new business reflected a plunge in demand for financial services and a further consumer slowdown, with a partial offset from a minor recovery in business services after a larger July drop – chart 3.

Chart 2

Chart 3

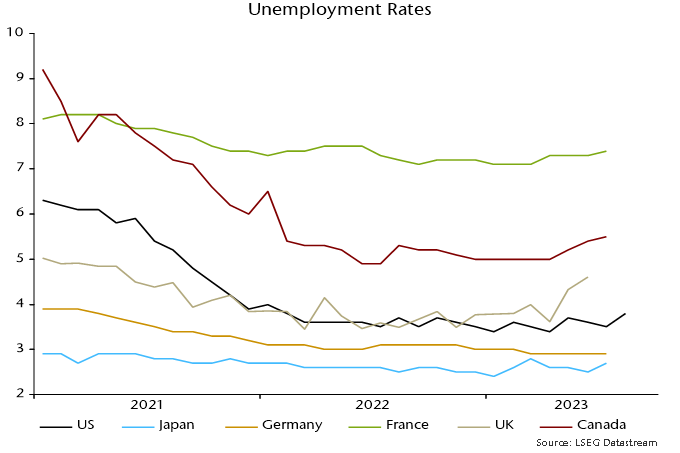

The ending of the services mini-boom, which fuelled recent employment gains, suggests a faster loosening of labour markets. Unemployment rates have reached 12+ month highs in the US, France, the UK and Canada, while a rise appears to be under way in Japan – chart 4.

Chart 4

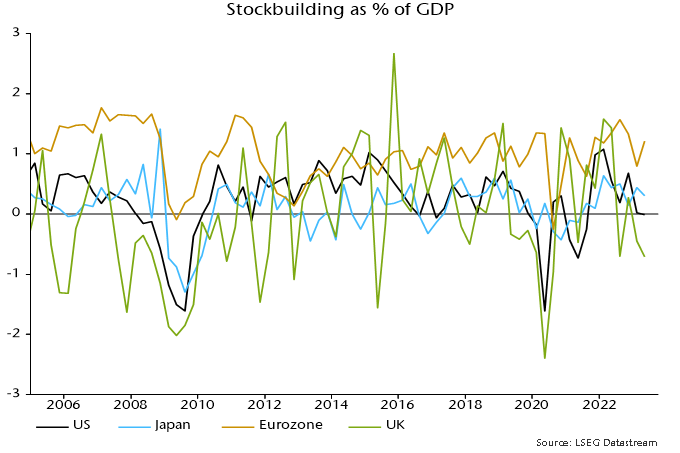

Previous posts suggested that a bottoming out of the stockbuilding cycle would support manufacturing new orders later in 2023. The cycle downswing, however, could be extended by delayed inventory cut-backs in the Eurozone: stockbuilding bounced back in Q2 as final demand contracted sharply, with recent adjustment lagging far behind the US / UK – chart 5.

Chart 5

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments (3)

Real yields and oil rising certainly adds to concerns over where this cycle bottom will be.

My suspicion is there is we aren't at nominal money growth lows yet. Mortgage lending in the US in particular looks very weak.

Will be interesting to see if Manufacturing PMI new orders bounce in H2 on end of destocking. Not sure mkt cares about services.

Would it be possible to have a more in depth look at the monetary trends and the outlook for economic growth in the US? The consensus has clearly shifted towards a soft landing (or even no landing) and imo this view is supporting global equity and credit markets. So very curious about your take on this