UK headline inflation fall improving economic prospects; "core" still sticky

Simon Ward

Simon Ward

Post a Comment

Post a Comment

The surprise fall in CPI inflation from 2.8% in May to 2.4% in June mainly reflects weaker food and fuel prices along with an early start to the summer sales. The latter effect should unwind in July while “good news” on food and energy prices may be nearing an end, with commodity markets rebounding strongly over the past month – the S&P / Goldman Sachs all-commodities index is up by 9.1% in sterling terms.

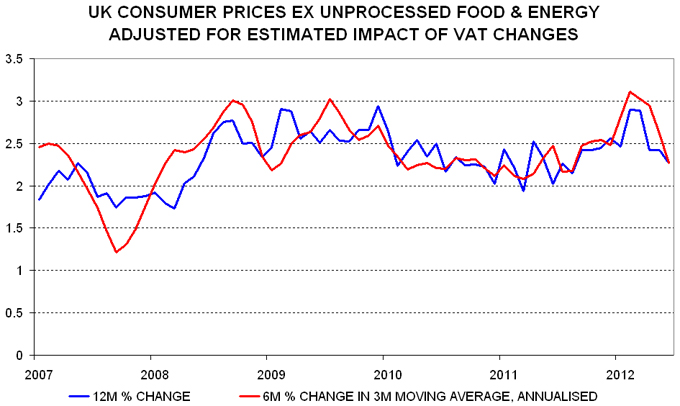

The annual change in “core” prices, as measured by the CPI excluding unprocessed food and energy, fell from 2.4% to 2.3%, with the decline attributable to the summer sales effect. Smoothed and seasonally adjusted, this index rose at a 2.3% annualised pace in the six months to June – see chart. Core pressures, in other words, remain inconsistent with the 2% inflation target, despite recent economic weakness.

The lower headline rate is improving economic prospects by contributing to a pick-up in real money supply expansion. Real non-financial M4 rose by 2.6% annualised in the six months to May, the fastest since April 2009, suggesting a return to respectable growth during the second half – see previous post.

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments