UK inflation slump piles pressure on tardy MPC

Simon Ward

Simon Ward

Post a Comment

Post a Comment

The forecast here a year ago was that the MPC would cut Bank rate to 0.5% during 2019. This was wrong in fact but right in spirit, as reflected in a significant downward shift in the yield curve.

The expected cut was probably pushed back by Brexit and election uncertainty but recent MPC communications and this week’s weak GDP and inflation data suggest that it will be delivered on the 30 January decision date.

The consensus thinks that a big enough bounce in January flash PMIs released next Friday could yet persuade the MPC to hold fire. This is doubtful and Tuesday’s labour market report may be more important – confirmation that employment has stalled and earnings growth is cooling would probably cement a January cut.

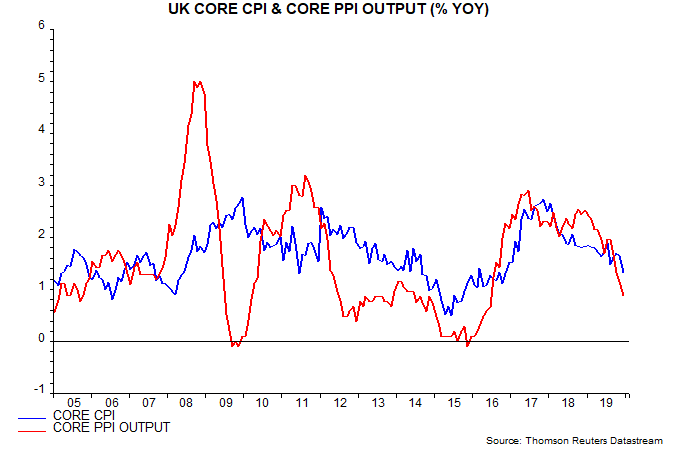

The volatile air fares component contributed to a decline in core CPI inflation to 1.4% (1.37%) in December, a three-year low, but there were also downward moves in food, non-energy industrial goods and recreational and personal services. A November post suggested that the core rate would fall further based partly on a lagged relationship with core producer output price inflation, which continued to plunge last month – see first chart.

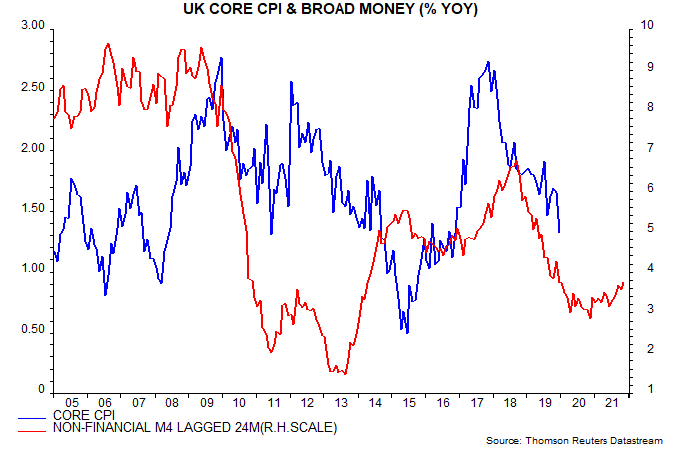

From a causal perspective, inflationary pressures are ebbing in lagged response to a fall in annual broad money growth – as measured by non-financial M4 – from nearly 7% in late 2016 to below 3% in late 2018: the monetarist rule of thumb is that money trends lead prices by about two years on average, although the relationship can be temporarily disrupted by large exchange rate swings (such as the post-EU-referendum depreciation) – second chart. The suggestion is that core inflation will continue to ease through 2020 barring a sizeable fall in sterling.

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments