Why has US bank loan growth surged?

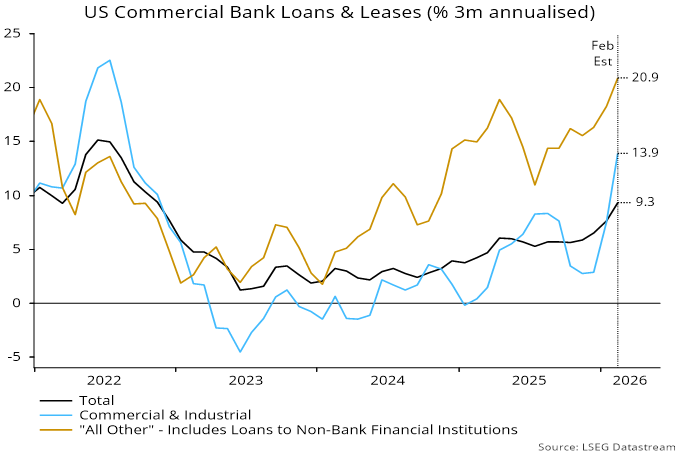

A recent pick-up in commercial bank loan growth is unlikely to be a positive signal for economic prospects.

Commercial banks’ loans and leases are estimated to have risen at a 9% plus annualised rate in the three months to February, up from 5.9% in the prior three months, based on weekly data through mid-month – see chart 1.

Chart 1

Unlike money measures, bank loans are a coincident or lagging indicator of economic activity. Commercial and industrial (C&I) loans and consumer installment credit are components of the US Conference Board lagging economic index.

The recent acceleration has been driven by two categories: C&I loans, which account for 21% of total loans and leases; and “all other”, accounting for 23%, which includes loans to non-bank financial institutions.

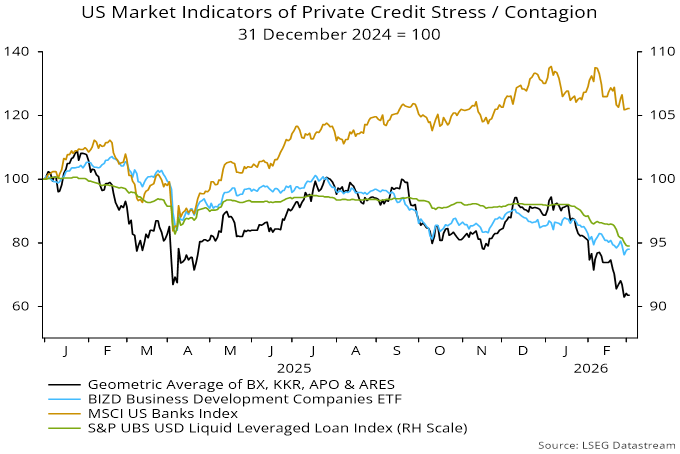

Growth of the latter category rose strongly over 2024-25 as banks contributed funding to a boom in private credit. Worries about credit quality and illiquidity have ended this boom, with market indicators signalling rising stress – chart 2. The recent further strength in “all other” loan growth may reflect private lenders drawing down bank credit lines as other sources of funding dry up.

Chart 2

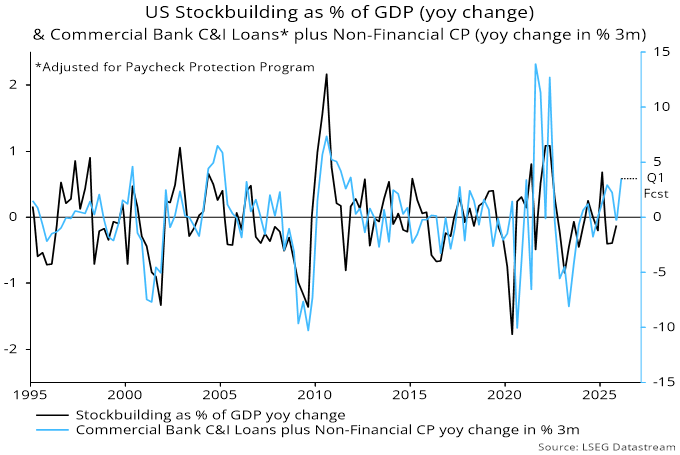

Reduced availability of private credit probably partly explains the pick-up in demand for C&I bank loans. However, such demand is also influenced by the stockbuilding cycle – chart 3. Stronger growth suggests that stockbuilding has rebounded in early 2026, supporting concurrent economic activity but with payback likely later in the year.

Chart 3

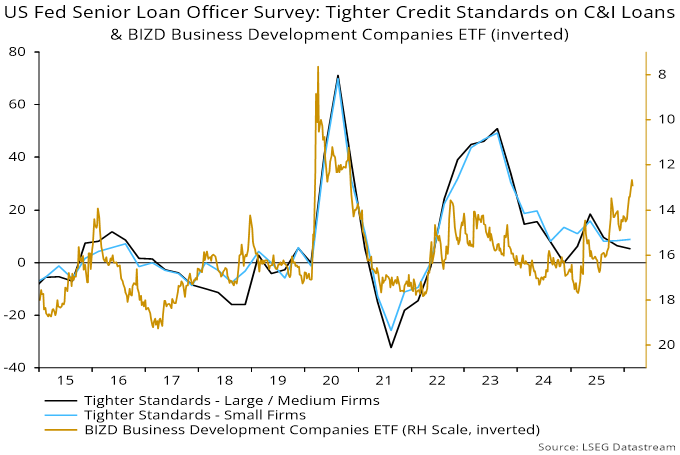

To the extent that bank loan acceleration reflects a “reintermediation” of credit demand due to a bust in private credit, it is likely to cause banks to tighten lending standards, with negative monetary and economic implications. Such tightening may be confirmed in the April Fed senior loan officer opinion survey released in early May – chart 4.

Chart 4