UK rates: the case for 50

The MPC’s slowness to cut rates risks aggravating a recent loss of economic momentum and prolonging an inflation undershoot.

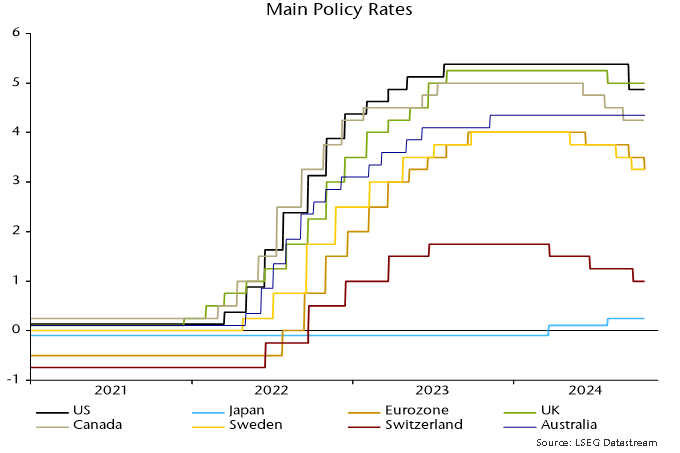

The expected 25 bp cut in November would be insufficient to catch up with reductions to date in the Eurozone, Sweden, Switzerland and Canada – see chart 1.

Chart 1

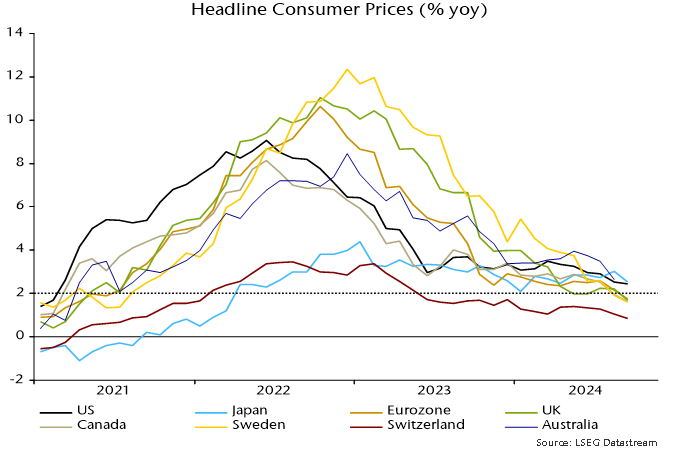

UK annual headline consumer price inflation is as low or lower than in all these jurisdictions except Switzerland – chart 2.

Chart 2

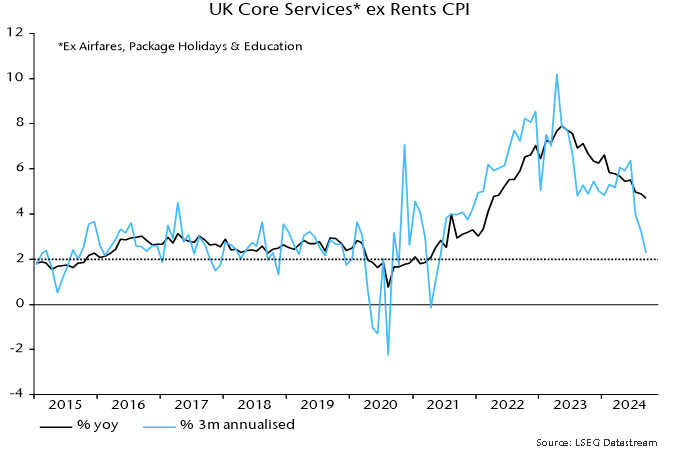

The MPC’s focus on the “core services” third of the inflation basket is misplaced. Monetary conditions determine aggregate inflation, with the component breakdown partly shaped by “exogenous” factors. A fall in energy prices and slowdown in food costs have suppressed headline inflation while allowing consumers to spend more on other items, delaying price deceleration in these areas.

This suggested that services disinflation would speed up as commodity prices stabilised or recovered, a development that appears to be playing out – chart 3.

Chart 3

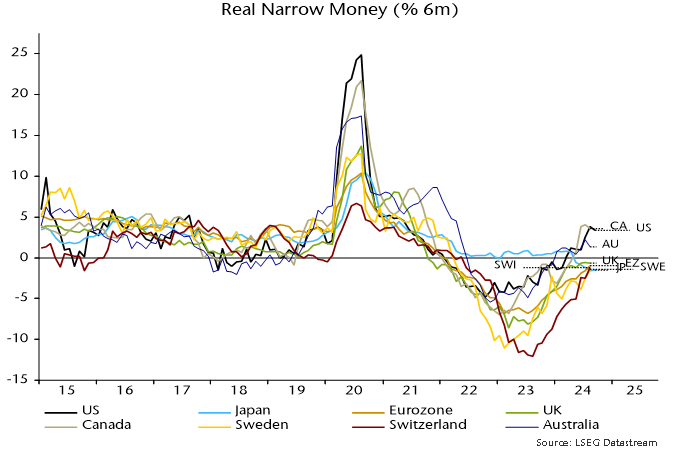

Six-month consumer price momentum continues to mirror the profile of broad money growth two years earlier, a relationship suggesting a further decline and extended undershoot of the 2% target. A recovery in six-month broad money momentum has stalled below the 4.5% pa level historically consistent with 2% inflation – chart 4.

Chart 4

UK six-month real narrow money momentum is negative and similar to levels in the Eurozone, Sweden and Switzerland, suggesting equally poor economic prospects – chart 5.

Chart 5

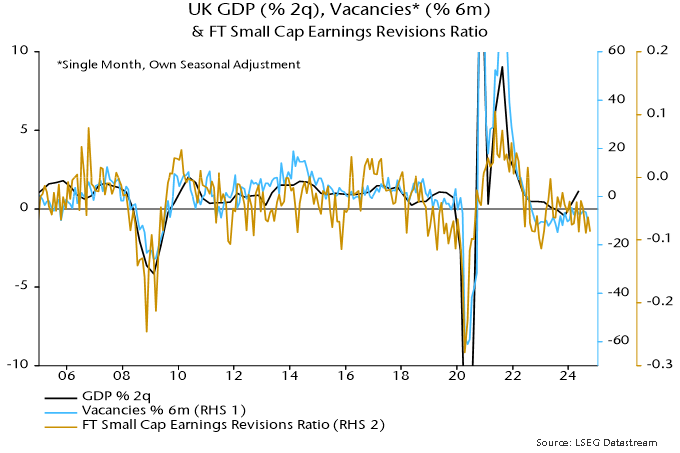

The double dip mooted in an earlier post could be under way. Recent signs of a loss of momentum include a faster rate of decline of job vacancies and an increase in small firm earnings downgrades – chart 6.

Chart 6

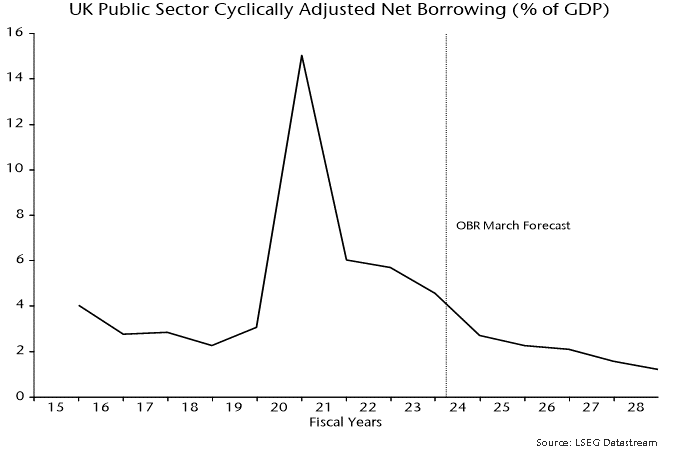

The previous government’s fiscal plans implied significant tightening in 2024 and 2025, according to the OBR – chart 7. Changes to the fiscal rules to be announced by Chancellor Reeves will allow for additional medium-term borrowing but are unlikely to alleviate near-term restriction.

Chart 7

It might be expected that the MPC would be especially sensitive to downside risks, following its mistake of responding too late in the opposite scenario in 2021-22 when inflation was starting to rip. Could confirmation of economic weakness and a restrictive Budget yet put a warranted 50 bp on the table for November?