More signs of Eurozone softening

Eurozone money trends have been giving a downbeat signal for economic prospects. Incoming evidence is consistent with a loss of momentum.

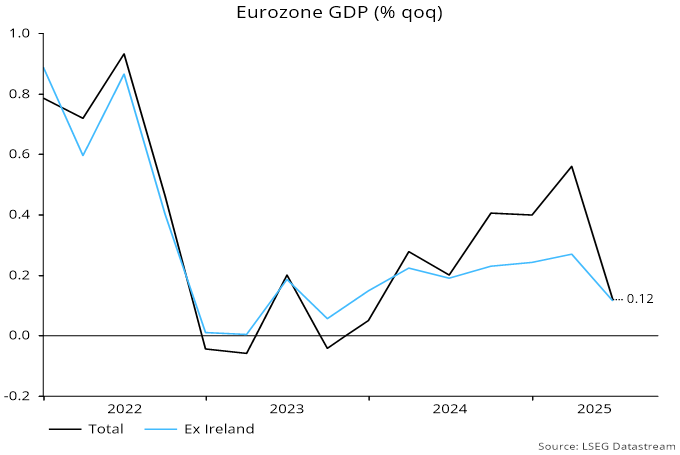

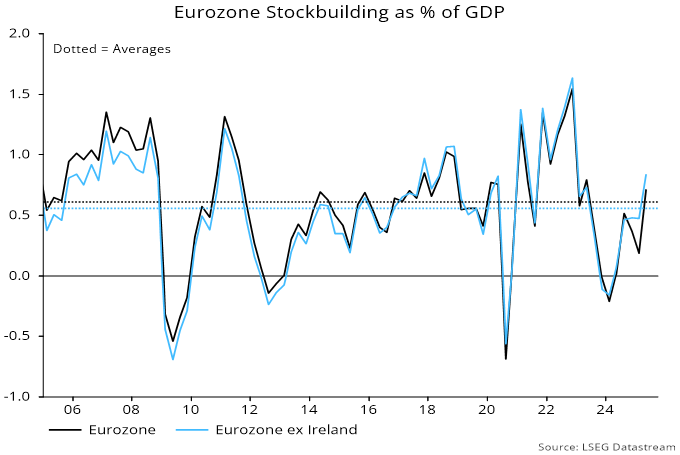

Eurozone GDP rose by only 0.8% at an annualised rate during H1 excluding distorted Irish numbers – see chart 1. Growth was dependent on an increase in stockbuilding, to an above-average level as a percentage of GDP – chart 2.

Chart 1

Chart 2

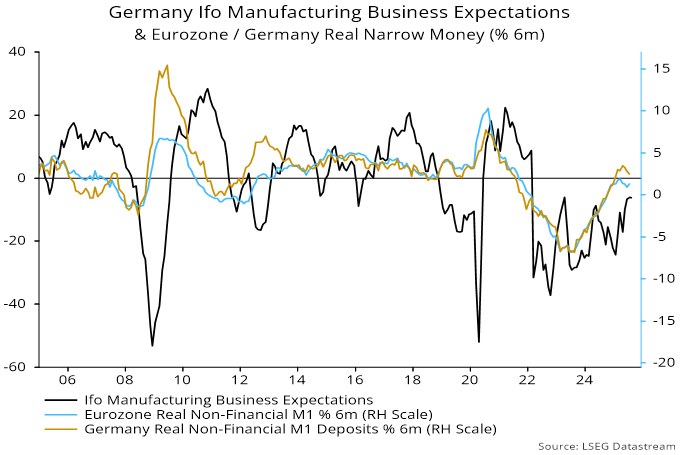

Rises in bond yields and the euro exchange rate have tightened monetary conditions, offsetting ECB rate cuts. Six-month Eurozone real narrow money momentum peaked in March, although the subsequent reversal has been modest – chart 3.

Chart 3

German Ifo manufacturing business expectations – closely correlated with Eurozone / German manufacturing PMIs – reached a two-year high in July, consistent with earlier monetary acceleration. Expectations moved sideways in August, with the March peak in real money momentum suggesting an inflection weaker soon.

Other evidence supports this forecast. The one-month change in the OECD’s German leading index also anticipates turning points in Ifo expectations and has eased since May – chart 4.

Chart 4

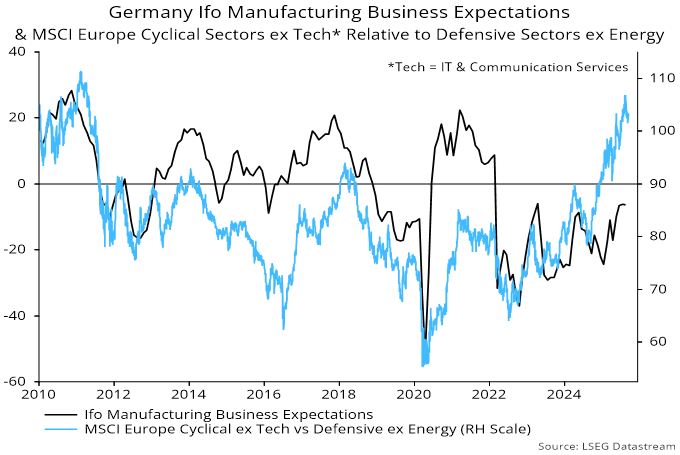

European cyclical sector equities often start to lag as business surveys inflect weaker and have given back some outperformance since mid-August – chart 5.

Chart 5

The Sentix and ZEW surveys of financial analysts correlate with Ifo results, with Sentix September numbers already available and showing a second monthly decline – chart 6.

Chart 6

The slowdown in Eurozone / German real money momentum is not yet alarming and may prove temporary, particularly if bond yields and the euro subside. Still, the ECB’s move to the sidelines was premature, with near-term data likely to bolster the case for further easing.