Is Eurozone labour market resilience about to crumble?

Recent Eurozone money trends cast doubt on economic optimism based on German / regional fiscal expansion. Weakening job openings suggest that a negative economic scenario is already starting to crystallise.

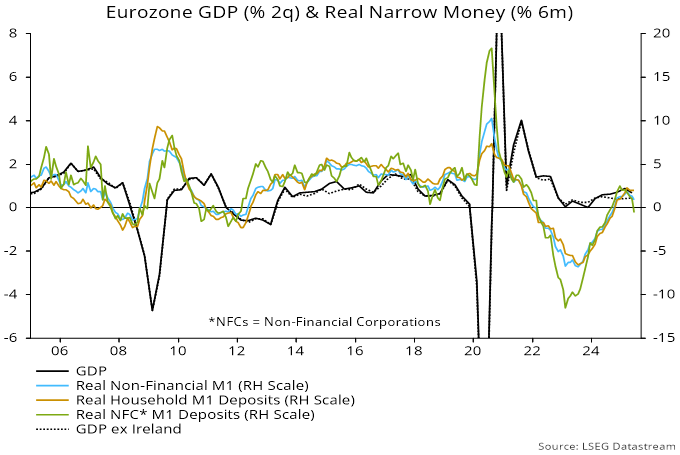

Six-month real narrow money momentum peaked in March at a modest level by historical standards, declining into June. The fall was driven by weakness in corporate deposits, suggesting that firms would cut back investment and hiring – see chart 1 and previous post for more discussion.

Chart 1

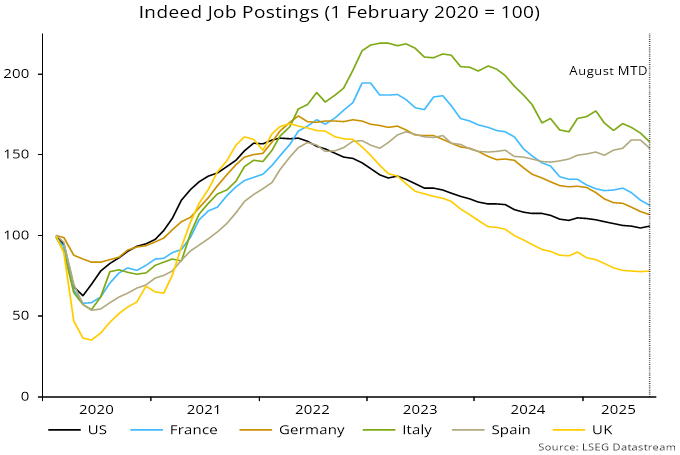

Indeed numbers on job postings are a timely coincident indicator of labour demand and appear to display less volatility than official survey-based measures of job openings or vacancies. The level and rate of decline of the UK Indeed series signalled recent job losses – chart 2.

Chart 2

The latest numbers show signs of stabilisation in the UK / US. By contrast, job postings in Germany and France are falling rapidly, with the Italian series breaking below its late 2024 low and even Spain rolling over.

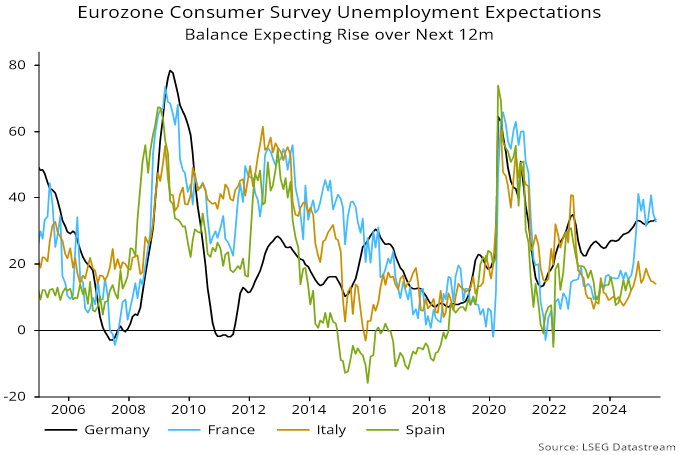

The German / French results chime with elevated consumer expectations of a rise in unemployment – chart 3*.

Chart 3

Why haven’t ECB rate cuts and German fiscal expansion energised the Eurozone economy? The initial impact of the fiscal news has been to push up longer-term yields and the euro, offsetting ECB stimulus.

Fiscal expansion, even if well-executed, will play out over the medium term, with growth implications dependent partly on the extent of monetary financing. The direct and confidence effects of the unfavourable US-EU trade “deal”, meanwhile, are a further near-term negative.

*The Spanish series has been suspended.

It definitely looks like more monetary easing is required ASAP. Yield curve steepening from a heavily inverted positions has also historically coincided with labour market weakness.