Global money update: tentative positive

The cycles framework used here suggests a window for global economic strength in H2 2025 / H1 2026 as the stockbuilding and business investment cycles move towards peaks – see previous commentary. This scenario, however, requires confirmation from a pick-up in global real money momentum into mid-2025.

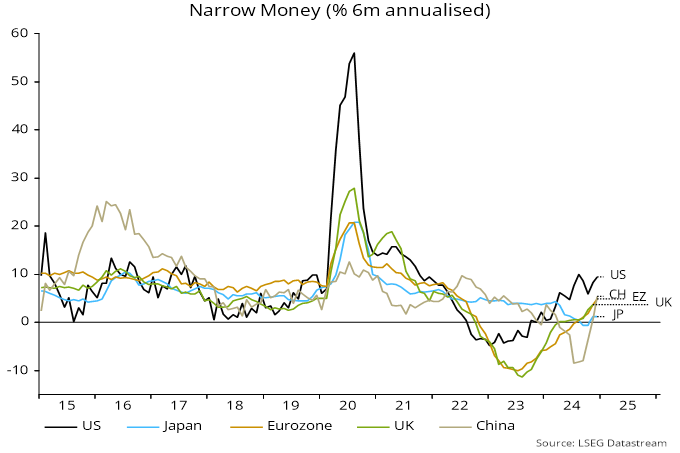

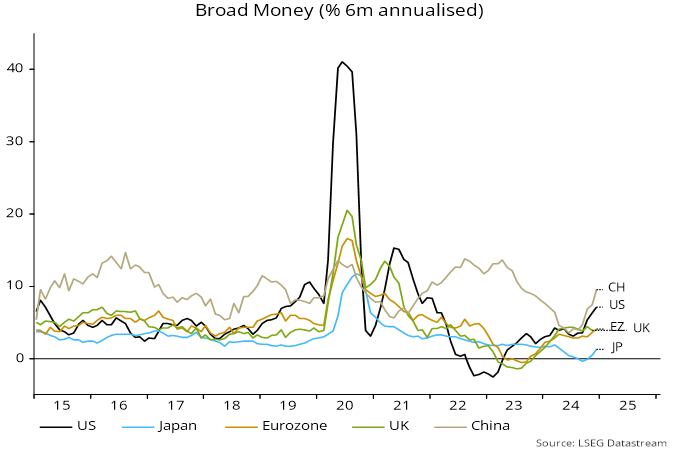

December money numbers are tentatively supportive. Six-month growth rates of narrow and broad money rose across the US, Japan, Eurozone and China – charts 1 and 2.

Chart 1

Chart 2

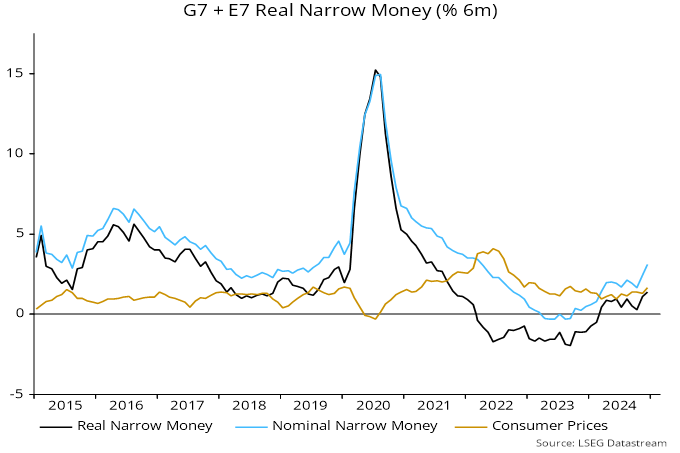

Based on monetary data covering 84% of the aggregate, global (i.e. G7 plus E7) six-month real narrow money momentum is estimated to have reached its highest since 2021 (October). The rise in nominal growth in December was partly offset by an energy-driven increase in six-month consumer price momentum – chart 3.

Chart 3

Several qualifications are in order. The positive signal from the recent pick-up relates to economic prospects for H2 2025, based on the usual six to 12 months lag. H1 performance is expected to be weak, reflecting stalled real narrow money momentum between April and October 2024.

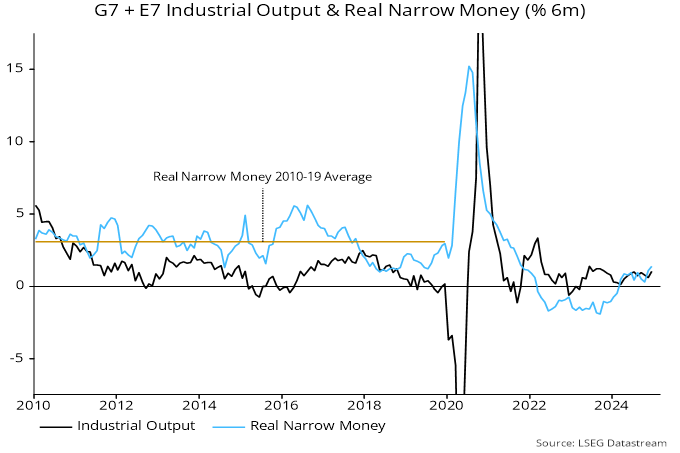

Real money momentum, moreover, remains low by historical standards. A rise at least to the 2010-19 average is necessary to validate a late 2025 / H1 2026 economic “boomlet” scenario – chart 4.

Chart 4

The rise in longer-term interest rates in the US and Europe since the start of December, meanwhile, could slow or reverse the money growth pick-up.

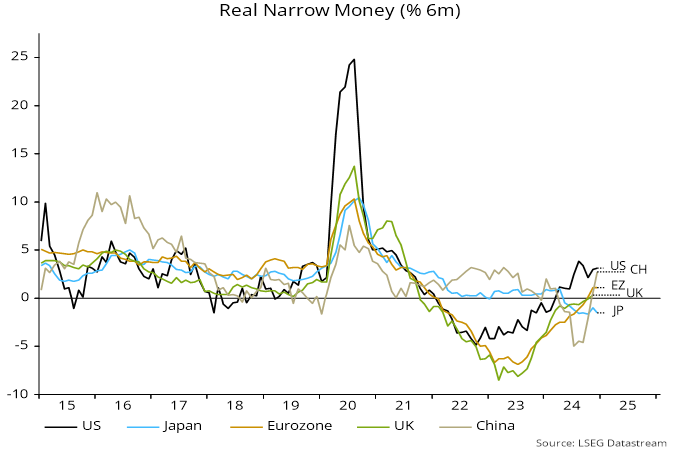

Despite rising in November / December, US six-month real narrow money momentum remains below its August peak. With China / Europe catching up, US economic and / or equity market outperformance may fade or reverse – chart 5.

Chart 5

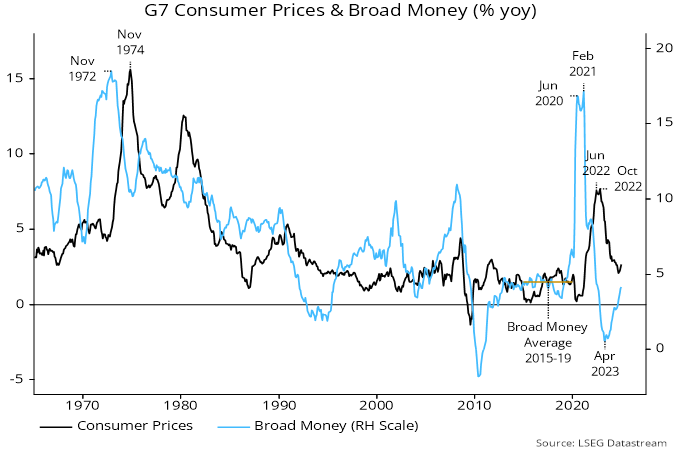

It is much too early to worry about a money growth revival fuelling another inflation pick-up. G7 annual broad money growth is still slightly below its average over 2015-19, a rate of expansion associated with below-target headline / core inflation outcomes – chart 6. The roughly two-year lag in the relationship suggests further downward pressure on inflation in 2025 and no serious upside threat before late 2026 at the earliest.

Chart 6