Global industrial momentum still weakening

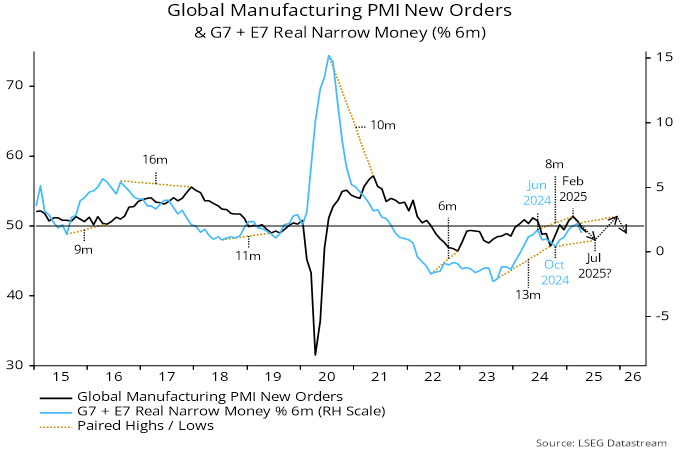

Global manufacturing PMI new orders – a timely coincident indicator of industrial momentum – fell for a third month in May. The decline from a February peak is consistent with a slowdown in global six-month real narrow money momentum between June and October 2024 – see chart 1.

Chart 1

The PMI fall started slightly earlier than had been expected here. The eight-month interval between the June peak in real money momentum and the February PMI peak compares with an average lag of 11 months at prior turning points since 2015.

Monetary considerations alone would suggest that the PMI will decline further into mid-year before recovering to another local high around end-2025 – the dotted arrows in the chart show a possible path.

The US trade policy shock, however, is likely to impart a negative skew to this profile, as recent demand front-loading reverses and spending decisions remain on hold until tariff uncertainty abates.

Accordingly, the current PMI decline could extend further than indicated with only a minor H2 recovery. Weak April money numbers, moreover, suggest darkening prospects for end-2025 – see previous post.