ECB policy easing is working

Whisper it softly but Eurozone economic prospects are improving.

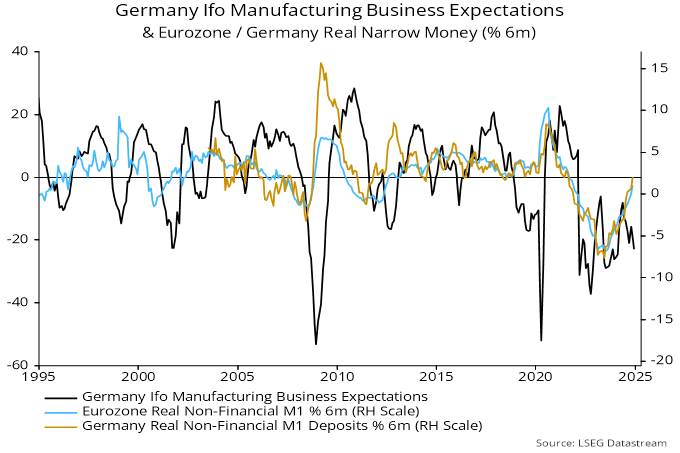

Six-month momentum of real non-financial M1 turned positive in October, reaching a three-year high in November. The recovery has been broadly-based across countries, with German momentum slightly above the Eurozone average – see chart 1.

Chart 1

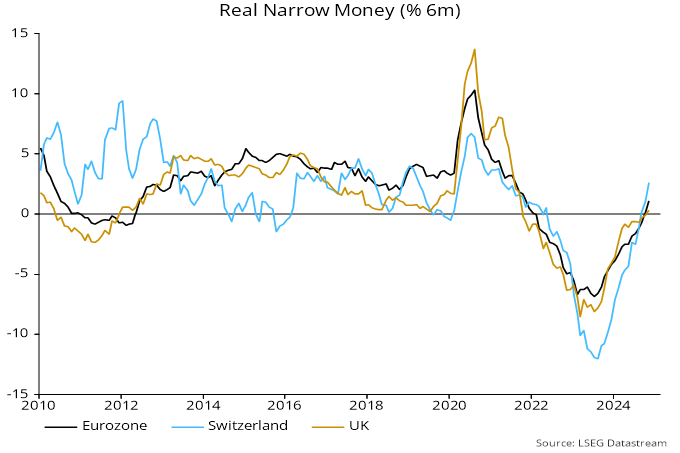

The sectoral breakdown shows that real M1 deposits of both households and non-financial corporations have returned to growth – in contrast to the UK, where corporate narrow money is still contracting, in nominal as well as real terms.

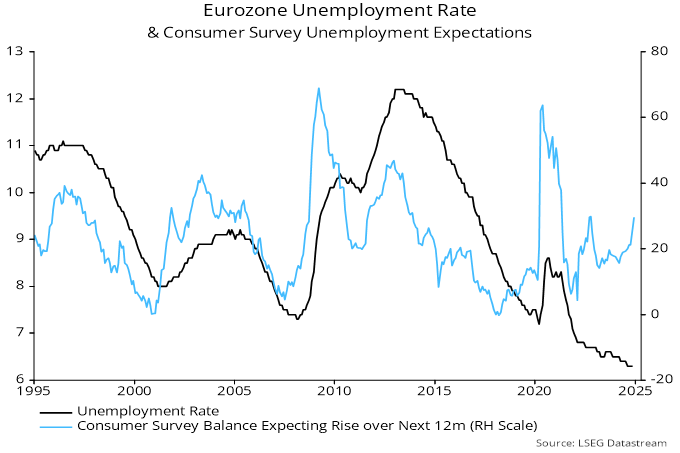

Economic news supports further policy easing. Six-month headline / core CPI momentum is close to target (2.1% / 2.2% annualised respectively in December) and there are signs of labour market softening, including a pick-up in consumer unemployment expectations – chart 2.

Chart 2

The Swiss National Bank started cutting rates in March, three months before the ECB, with the cumulative reduction now 125 bp versus 100 bp in the Eurozone. Swiss six-month real narrow money momentum is stronger and likely to be matched by the Eurozone soon – chart 3.

Chart 3

The UK is lagging because the backward-looking MPC started later with cuts of only 50 bp. A stall in six-month real narrow money momentum from last spring signalled that the economy was heading for renewed stagnation well before the end-October Budget.

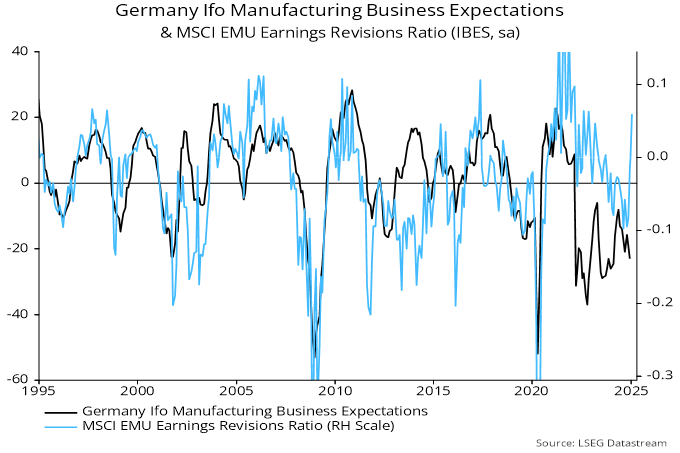

Improving Eurozone economic prospects may partly explain a spate of upgrades to corporate earnings forecasts by equity analysts. A positive January revisions ratio contrasts with negative readings in the US / UK and supports the monetary suggestion of a recovery in manufacturing surveys – chart 4.

Chart 4