Alarming Eurozone / UK money data

Eurozone and UK April money numbers signal rising recession risk and suggest that policy-makers should be considering easing not tightening.

Three-month annualised growth of Eurozone narrow money – as measured by non-financial M1 – slumped from 5.3% to 1.5% between January and April. UK growth fell from 3.8% to 0.7% over the same period, with a large contraction in April alone.

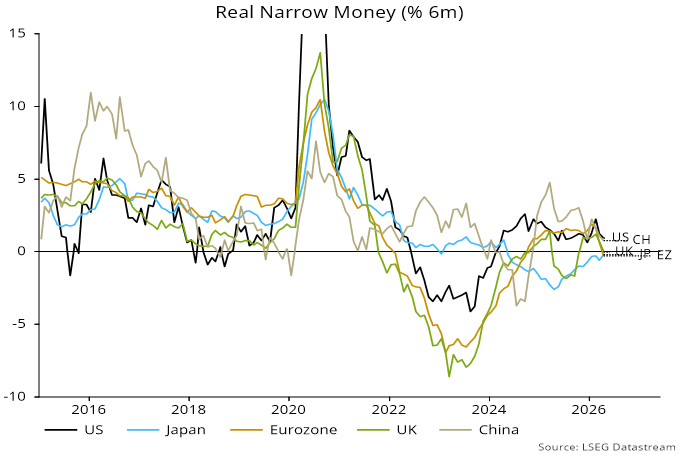

The nominal slowdowns compound a squeeze on real money from consumer price acceleration due to the Gulf War III supply shock. Six-month momentum of real narrow money fell to zero in the UK in April while turning negative in the Eurozone – see chart 1.

Chart 1

Real money contractions have been a recession warning signal historically. An obvious push-back is that much greater weakness in 2022-23 was not reflected in a subsequent economic slump. Negative momentum was a misleading indicator of monetary conditions then because of a large overhang from the 2020-21 money growth surge. There is no such overhang now, so dismissing current weakness on the basis of that experience is dangerous.

Broad money trends are also worrying, with nominal growth of only 3.5% and 3.6% annualised respectively in Eurozone non-financial M3 and UK non-financial M4 in the three months to April. US broad money, by contrast, expanded at a 7.6% pace over the same period (M2+ measure).

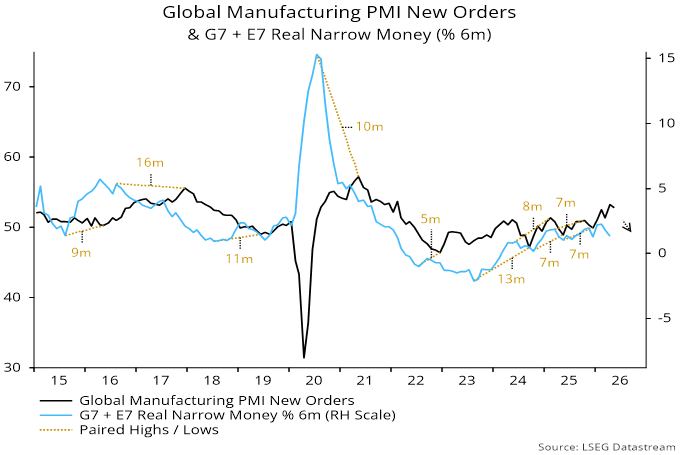

Globally, six-month real narrow money momentum fell for a second month in April, supporting the forecast of a fall in manufacturing PMI new orders during H2 – chart 2.

Chart 2