Why is the UK an employment outlier?

UK monetary trends have been arguing for faster MPC easing. Labour market news is now reinforcing the message.

Employment developments appear notably weaker in the UK than in other major economies. The PAYE payrolled employees series fell by 0.09%, 0.15% and a provisional 0.11% in February, March and April respectively. These declines are the equivalent of falls in US non-farm payrolls of 140k, 240k and 170k.

US payrolls, of course, have risen respectably year-to-date, while Eurozone employment grew by 0.3% in Q1.

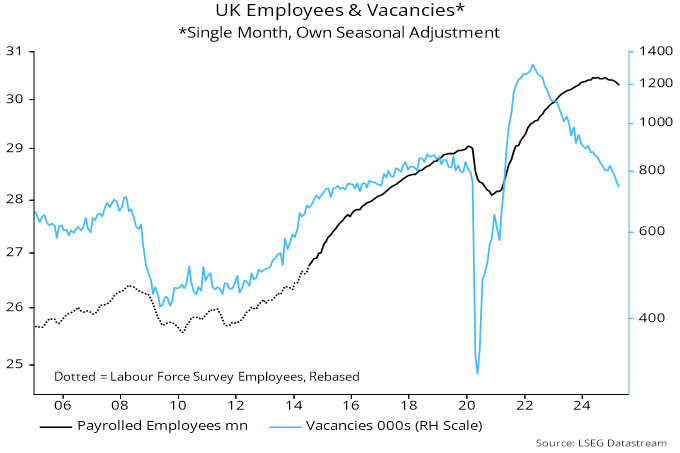

The February-April UK payrolls contraction followed a pick-up in the rate of decline of the official single-month vacancies series (seasonally adjusted here), which has fallen to its lowest level since 2016 – see chart 1.

Chart 1

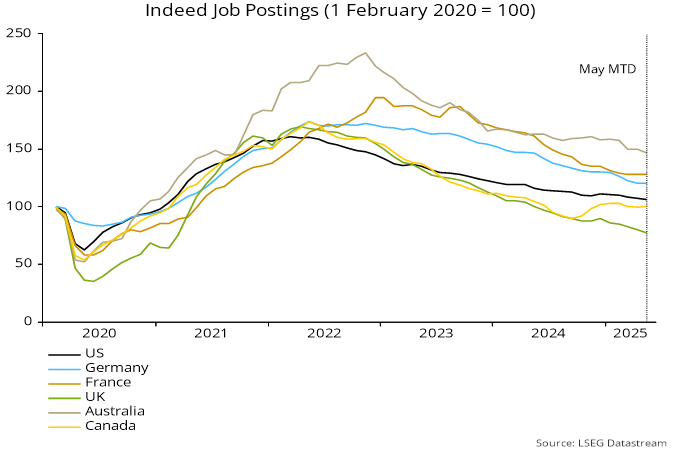

Indeed job postings numbers closely track the official vacancies series and have declined further so far in May – chart 2. The Indeed numbers have fallen by more in the UK than elsewhere, to a lower level relative to the pre-pandemic (February 2020) starting point – chart 3.

Chart 2

Chart 3

UK underperformance may be partly attributable to government-imposed rises in labour costs, in the form of the increases in employer national insurance and the minimum wage, and prospectively via the Employment Rights Bill.

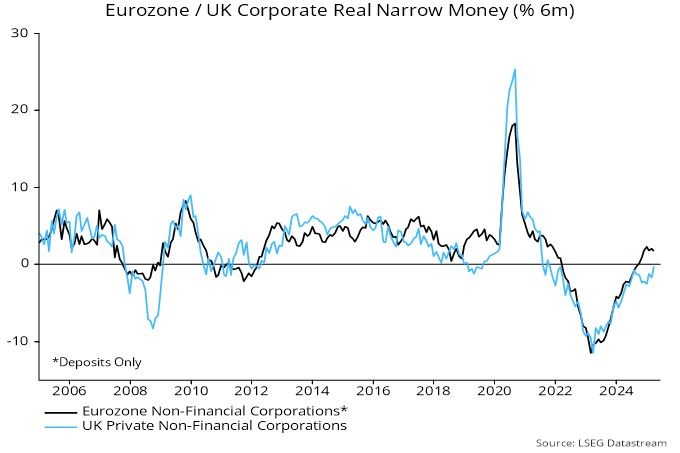

Pessimism here about employment prospects, however, also reflected weak corporate money trends. The six-month rate of change of real M1 holdings of non-financial corporations has remained negative, in contrast to a rise into solid positive territory in the Eurozone – chart 4.

Chart 4

Relative money weakness suggested that UK firms were under greater financial pressure to cut costs than their Eurozone counterparts.

A hopeful sign is that UK six-month corporate real money momentum has recovered recently, narrowing the gap with the Eurozone. A key issue is whether this revival is sustained as the NI and minimum wage hikes take effect.

UK employment weakness appears at odds with Q1 GDP “strength”. The UK quarterly numbers, however, have been volatile and year-on-year growth of 1.3% in Q1 is little different from the Eurozone (1.2%).

Front-running of US tariffs temporarily boosted GDP in the rest of the world last quarter. US real imports rose by 10.8%, equivalent to 1.4% of US GDP, between Q4 and Q1. GDP in the rest of the world is 2.7 times the US level measured at current market prices and 5.8 times based on purchasing power parity. Depending on which divisor is used, the US imports increase implies a 0.25-0.5% lift to GDP elsewhere.