Weaker US / Eurozone money data

US / Eurozone January money numbers suggest that US policy chaos is damaging economic prospects.

The narrow money measures followed here – US M1A and Eurozone non-financial M1 – were unchanged and fell on the month respectively. Narrow money weakness can reflect reduced confidence and spending intentions.

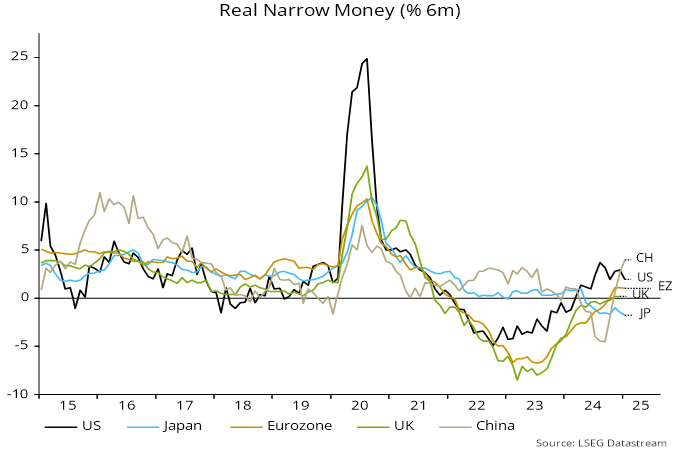

US six-month real narrow money momentum fell between August and October, partially recovered into year-end but has now returned to the October level – see chart 1. The slowdown since August signalled recent softer economic data – see previous post.

Chart 1

A recovery in Eurozone six-month real narrow money momentum stalled in December / January but the gap with the US has narrowed significantly since August, suggesting better relative performance.

US narrow money momentum may weaken further. Policy chaos may cause spending to be deferred, reducing demand for transactions money.

The Fed has gone on hold with rates judged still to be in restrictive territory. The ECB has cut by more, is still in easing mode and may be closer to “neutral”.

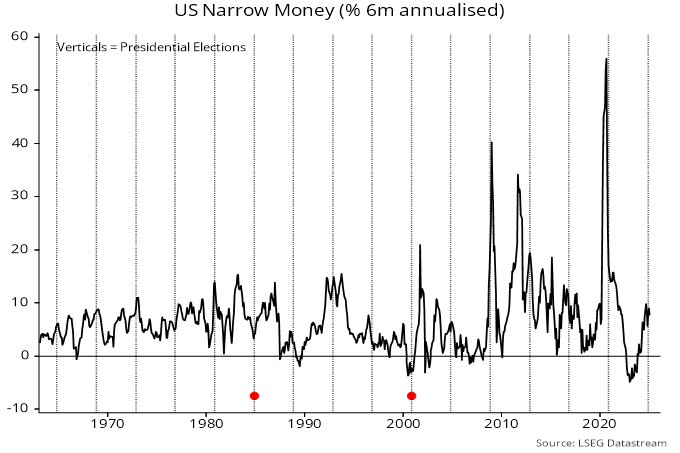

A further consideration noted previously is that US narrow money growth has tended to rise into presidential elections but reverse shortly before or after the poll date – chart 2. (1984 and 2000 were notable exceptions.)

Chart 2

It’s just the typical US election cycle monetary gyrations? In this case, the fiscal deficit also rose markedly, especially in October & November where it was $624bn combined.

Monetary policy is far too tight in US / EU and another temporary rise in inflation and its lagging nature could further delay significant easing.