UK money update: misleading M4ex

UK monetary alarm bells are ringing louder.

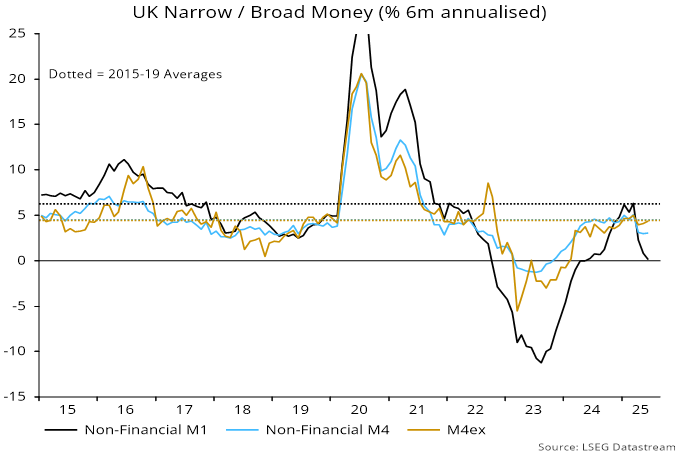

Six-month growth of the preferred narrow money measure here – non-financial M1, comprising holdings of households and private non-financial corporations (PNFCs) – fell further in June, to just 0.1% annualised. Growth of its broad equivalent, non-financial M4, remained at 3.0%, below a 4.5% average over 2015-19, associated with beneath-target average CPI inflation – see chart 1.

Chart 1

Monetary warning signals are being ignored partly because official / consensus focus is on the Bank of England’s headline M4ex broad aggregate, which grew by 4.4% annualised in the six months to June – exactly in line with its 2015-19 average.

M4ex relative strength, however, reflects rapid expansion – by 14.1% annualised in the six months to June – of money holdings of “non-intermediate other financial corporations (OFCs)”, mainly attributable to increases in balances of securities dealers and fund managers. Such holdings are volatile and – unlike non-financial M1 / M4 – uncorrelated with future activity / prices*.

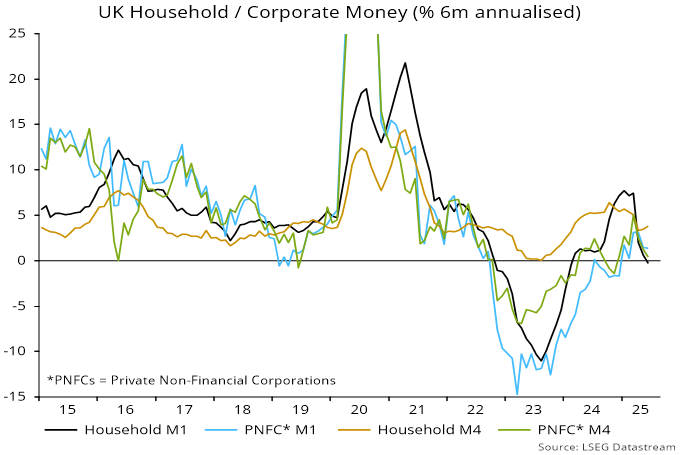

Six-month growth of M1 / M4 holdings of private non-financial corporations (PNFCs) fell further in June, to 1.4% / 0.4% annualised respectively. Household M4 growth firmed to 3.8% but M1 momentum moved into marginal contraction. The shift from sight deposits into time deposits and ISAs suggests weak spending intentions and a preference for saving – chart 2.

Chart 2

A previous post argued that falls in six-month non-financial M1 / M4 growth in April / May were partly payback for upward distortions related to portfolio adjustments before the October Budget and a front-loading of housing market activity ahead of the end of the stamp duty holiday. With such effects fading, ongoing monetary weakness is stronger evidence of overrestrictive policy.

*Correlations of the two-quarter rate of change of nominal GDP with two-quarter changes in money measures, lagged two quarters, over 1998-2019: M4ex +0.19, non-financial M4 +0.41, M4 of non-intermediate OFCs -0.08, non-financial M1 +0.65.

Monetary policy is too tight.The Labour market is much weaker than the BoE thinks.

Arguably fiscal policy is too loose, is supporting inflation and has prevented earlier rate cuts. Similar dynamics may be playing out elsewhere as well.