Global money update: slowdown on pause

The suggestion from cycle analysis of significant economic weakness in 2026-27 has yet to receive confirmation from monetary trends.

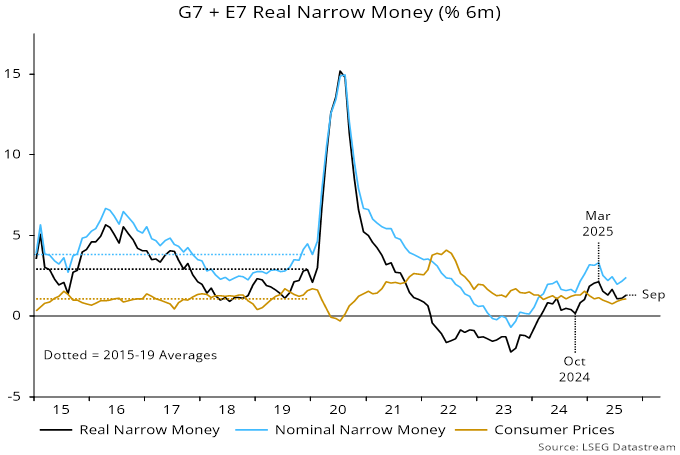

Global six-month real narrow money momentum recovered for a second month in September, though remains below a March peak. Nominal money growth firmed in August-September, offsetting a small rise in six-month consumer price momentum – see chart 1.

Chart 1

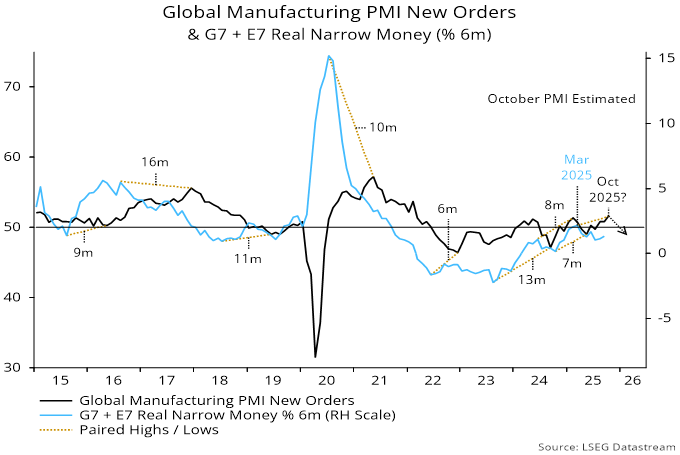

The March peak was expected here to be reflected in a peak in global manufacturing PMI new orders around October. DM flash results are consistent with a further rise in the orders index this month – chart 2.

Chart 2

The latest monetary numbers suggest that the expected PMI fall will be contained, at least through Q1 2026. This is compatible with cycle analysis: the stockbuilding cycle is judged to be at the start of a downswing, so the maximum negative impact could be delayed until H2 2026 or even later.

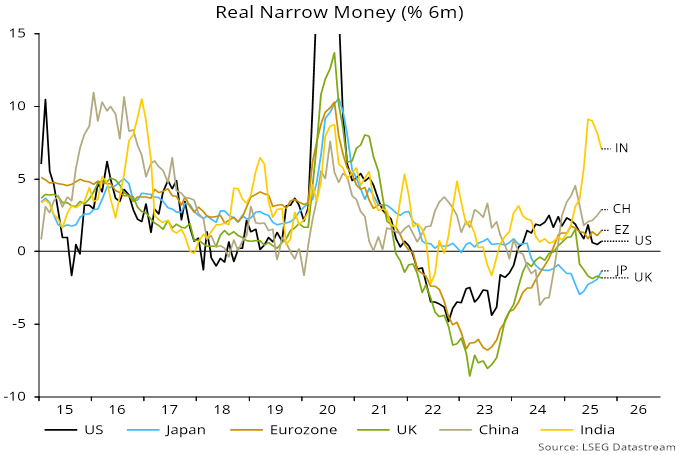

The minor recovery in global real narrow money momentum since July has been driven by China and Japan, with US, Eurozone and UK readings little changed and Indian growth moderating – chart 3.

Chart 3

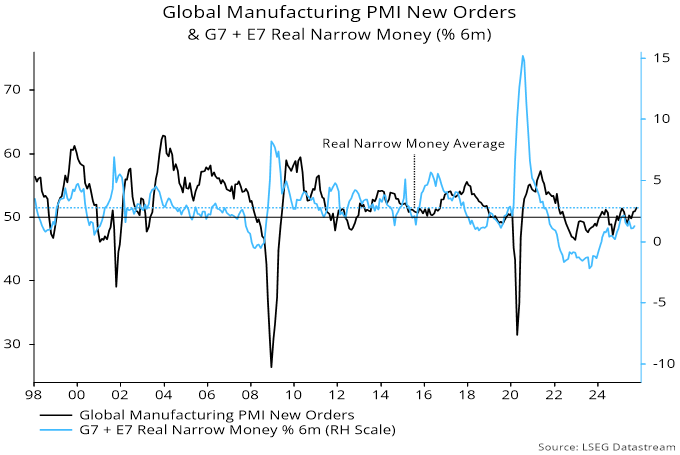

Real money momentum remains below its long-run average – chart 4.

Chart 4

Could recent / prospective central bank easing sustain monetary reacceleration, extending economic cycles? While possible, there are also reasons for expecting renewed monetary weakness.

First, policy stances are mostly still restrictive, and real rates may fall by less than nominal as inflation declines further.

Secondly, recent issues in private credit may cause banks to slow lending to shadow banks and tighten standards more generally, dampening (broad) money growth.

Thirdly, money trends reflect as well as influence economic cycles. Stockbuilding cycle downswings are associated with reduced demand for short-term business credit, which could contribute to monetary weakness.

Finally, the demand to hold narrow money is related to consumer / business confidence and spending intentions. Labour market weakness could lead to greater consumer caution, while ongoing trade dislocation and policy uncertainty may dampen business animal spirits.

I think a muddle through scenario, where extremely aggressive pro cyclical fiscal policy supports money growth, could persist for several years more.

Unemployment may not rise quickly, rather a slow grind upwards until that puts more pressure on credit or other economic stress points. Only then would this cycle end.