Global money update: renewed weakness

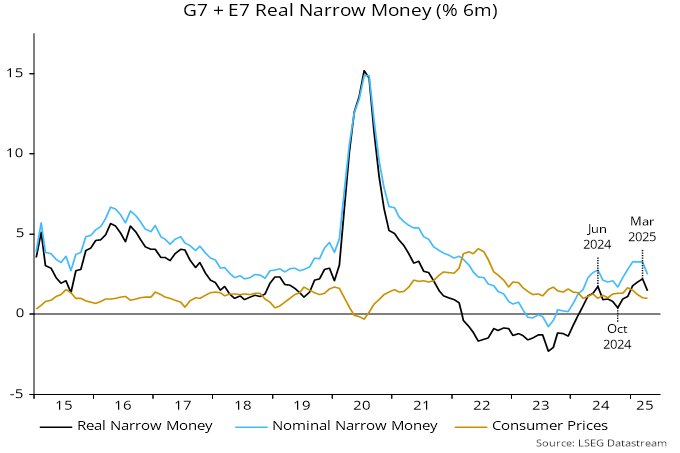

Global (i.e. G7 plus E7) six-month real narrow money momentum – a key leading indicator in the approach followed here – fell sharply in April, to its lowest level since December. The relapse douses hope generated by a pick-up into March, which suggested a bounce-back in the global economy later in 2025, assuming no further negative “shocks”.

The April fall was driven by a slowdown in nominal money growth to its weakest since November. Six-month consumer price momentum eased slightly further to match its 2024 low (2.0% annualised) – see chart 1.

Chart 1

To recap, a fall in real narrow money momentum between June and October 2024 was expected here to be reflected in a global economic slowdown in Q2 / Q3 2025, which the US trade policy shock will amplify.

Subsequent monetary reacceleration into March held out the hope of an economic recovery in late 2025, by which time negative tariff effects could be starting to fade.

The April money growth fall, however, suggests that a negative feedback loop is developing, with reduced confidence due to US policies resulting in increased risk aversion and a tightening of monetary conditions, despite most central banks remaining on an easing path.

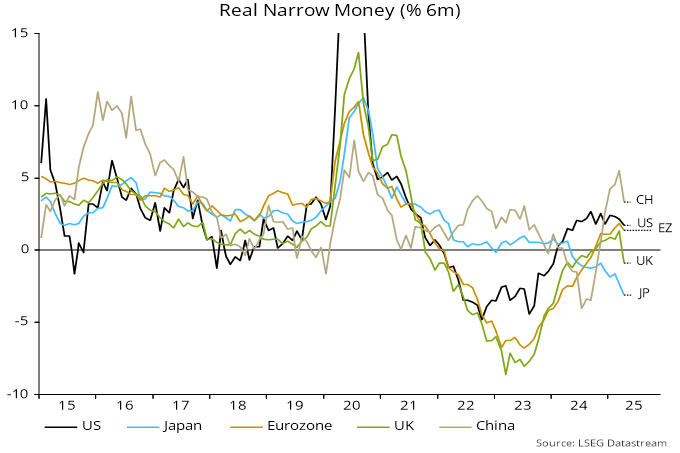

The April decline reflected falls across major economies, reinforcing the negative signal – chart 2.

Chart 2

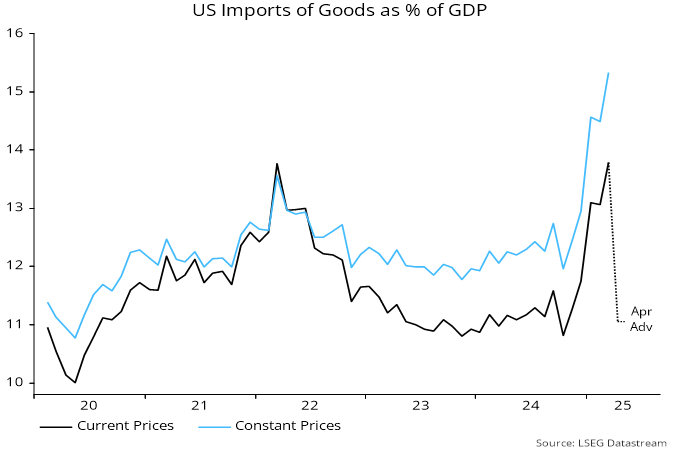

Economic momentum has been supported by demand front-loading but payback is arriving.

A surge in US goods imports boosted GDP in the rest of the world by 0.25-0.5% in Q1 but April advance numbers suggest a full reversal – chart 3.

Chart 3

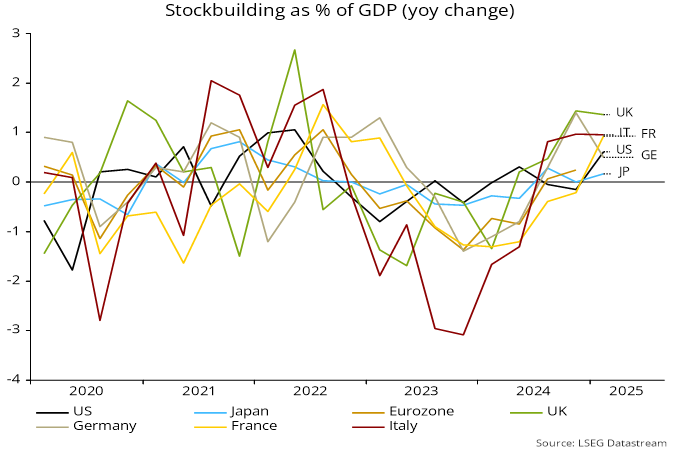

Inventory accumulation isn’t just a US story. Stockbuilding as a percentage of GDP rose similarly or by more in major European economies in the year to Q1 – chart 4.

Chart 4

Economic growth depends on the change in stockbuilding, so even a stabilisation at its recent pace would suggest a significant loss of output momentum.