Global money update: inflation squeeze

Global six-month real narrow money growth fell in March and is on course to decline further in April-May, suggesting a loss of economic momentum during H2.

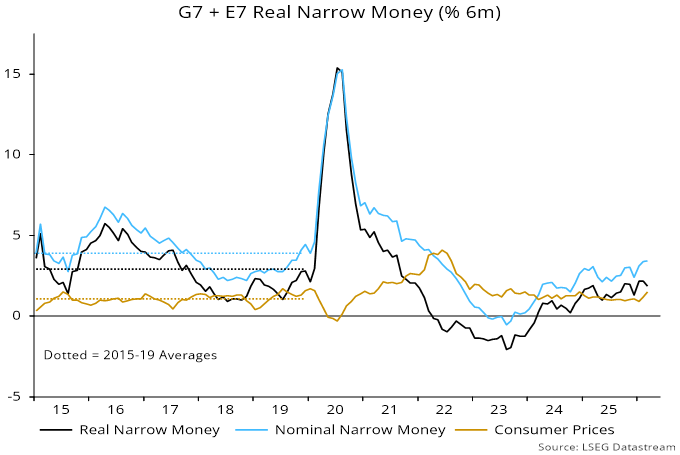

The March fall from a four-plus-year high in January / February was due to a pick-up in six-month consumer price momentum, with nominal money expansion unchanged – see chart 1.

Chart 1

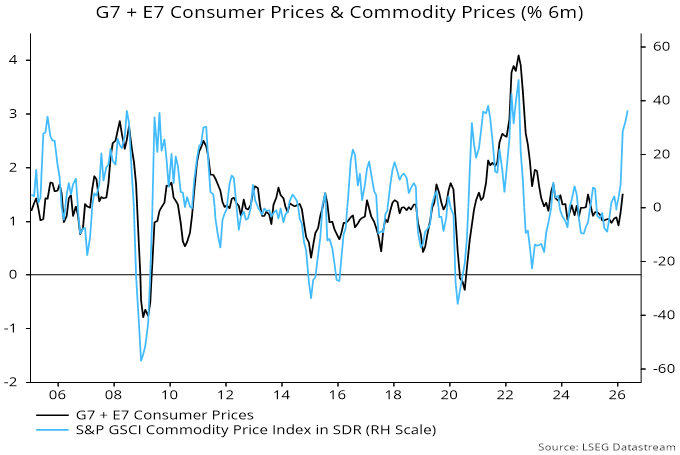

Commodity price strength implies a further increase in CPI momentum through May, at least – chart 2. So the slowdown in real money growth will extend unless nominal expansion accelerates – unlikely given recent upward pressure on rates.

Chart 2

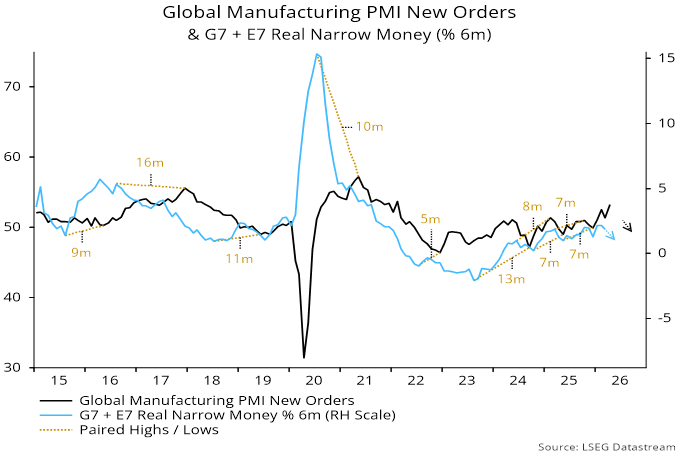

The earlier rise in real money growth has been reflected in a pick-up in global industrial momentum, with April manufacturing PMI new orders also the highest for four-plus years – chart 3. Orders have received an additional boost from precautionary stockpiling triggered by Gulf War III.

Chart 3

The lead time between turning points in real money momentum and PMI new orders has recently been running at seven months, suggesting a PMI reversal from September. The stockbuilding boost may have accelerated strength, however, implying an earlier peak.

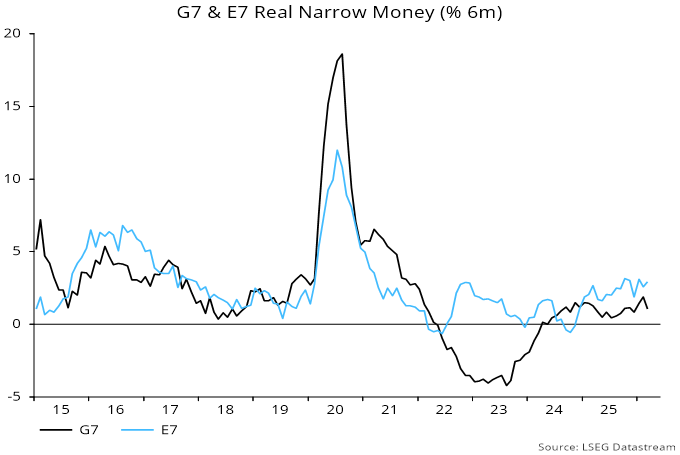

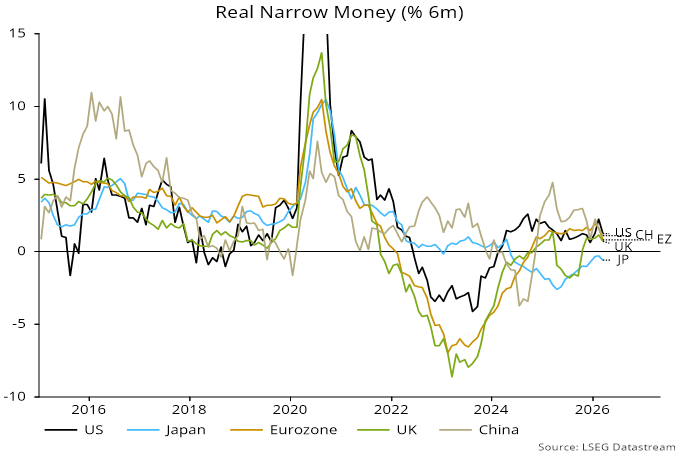

The March fall in global six-month real narrow money growth was driven by the G7 component, with E7 expansion tracking sideways – chart 4.

Chart 4

US growth fell in March but remains higher than in the rest of the G7 – chart 5.

Chart 5

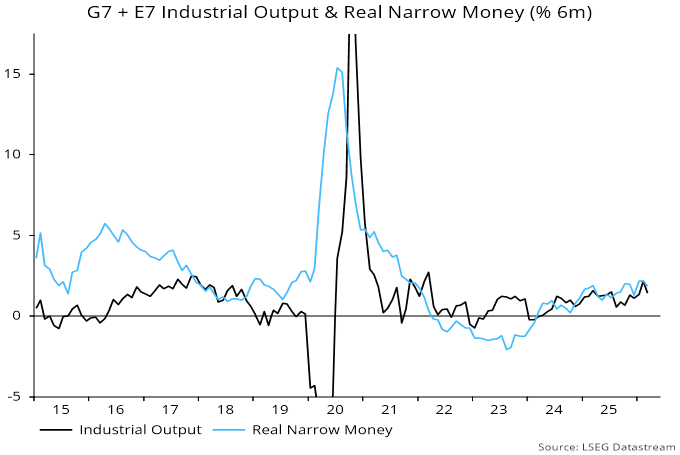

The March fall in global six-month real narrow money growth is estimated to have been accompanied by a similar slowdown in industrial output expansion, implying a continued small lead for the former – chart 6. The suggestion of “excess” money support for markets is consistent with recent equity market resilience.

Chart 6

The expected further fall in real money growth, however, and near-term support for output from full order books, could result in the series converging or crossing soon.