Global industrial momentum peaking on schedule

The forecast of a local peak in global industrial momentum – proxied by the manufacturing PMI new orders index – around end-Q1 appears to be on track. Monetary trends suggest a modest pull-back over Q2 / Q3 followed by renewed strength in late 2025. US policy actions threaten more pronounced and sustained weakness.

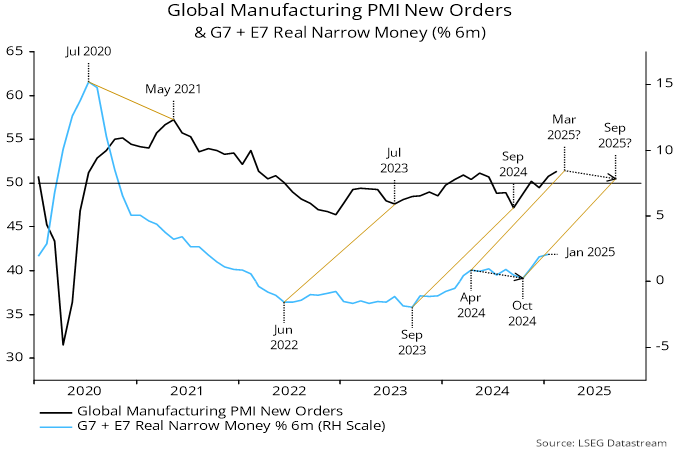

Global manufacturing PMI new orders rose further in February, moving above last year’s May peak to reach the highest level since March 2022 – see chart 1.

Chart 1

The upswing from a low last September, on the view here, reflects a rise in global six-month real narrow money momentum between September 2023 and April 2024 – turning points in money momentum have led the PMI by 10-13 months in recent years.

Real money momentum, however, eased between April and October 2024 before rising to new highs more recently. The suggestion was that the industrial pick-up would pause over spring / summer 2025 but strengthen further into 2026.

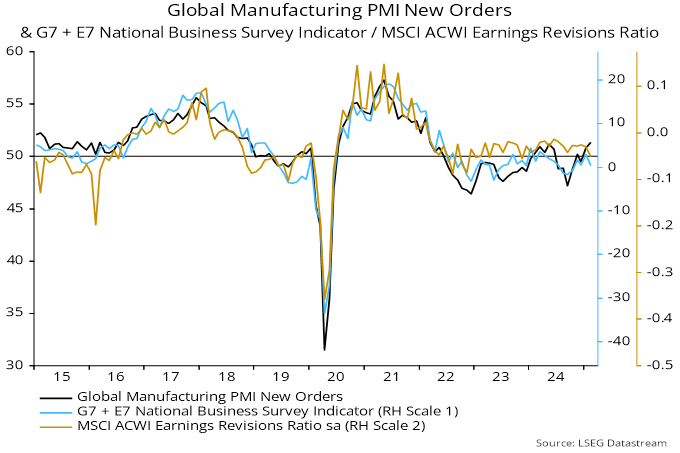

The view that the PMI new orders index is at or close to a peak is supported by a February fall in an alternative indicator combining forward-looking components of national business surveys (ISM for the US, NBS for China, Ifo for Germany etc.) – chart 2.

Chart 2

The global earnings revisions ratio also exhibits a contemporaneous correlation with the PMI and declined last month.

The baseline scenario of a modest PMI correction followed by renewed strength has, of course, been called into question by recent US policy actions.

Monetary trends are, for the moment, still giving a reassuring message, with global six-month real narrow money momentum rising slightly further in January – chart 1.

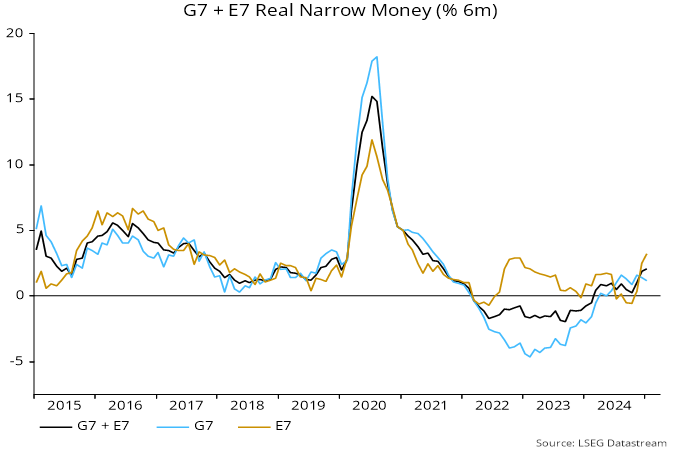

This increase, however, was due to additional strength in China, with US / Eurozone narrow money measures stalling in January, as previously discussed. In contrast to the global (i.e. G7 plus E7) measure, G7 six-month real money momentum has been moving sideways since August – chart 3.

Chart 3

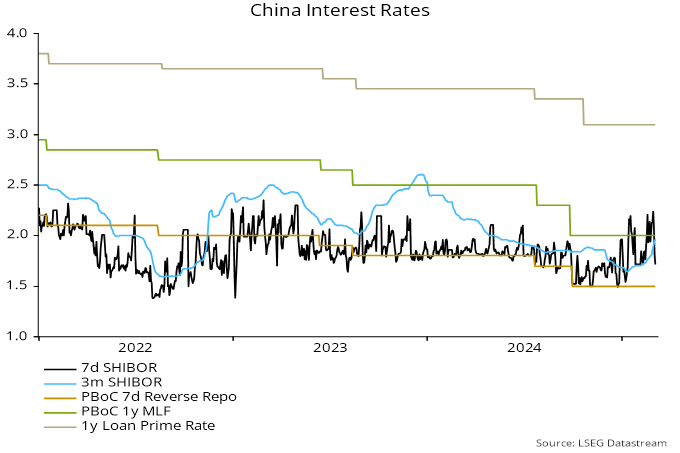

A recent back-up in Chinese money market rates, meanwhile, could presage less upbeat monetary data – chart 4.

Chart 4

A renewed fall in global real narrow money momentum would suggest more lasting / self-reinforcing damage from the US policy shock.

10y-3m has been behaving like it did every other cycle in the modern era.

More pronounced weakness, ie a recession will lead to more aggressive rate cuts and aggressive steepening.

The cyclical question is the push pull between late cycle inflation and weakening labour markets. This cycle has been fogged by extreme fiscal policy.