Chinese money update: steady as she goes

Chinese money trends suggest a continuation of sluggish economic growth, negligible inflation and a supportive liquidity environment for markets.

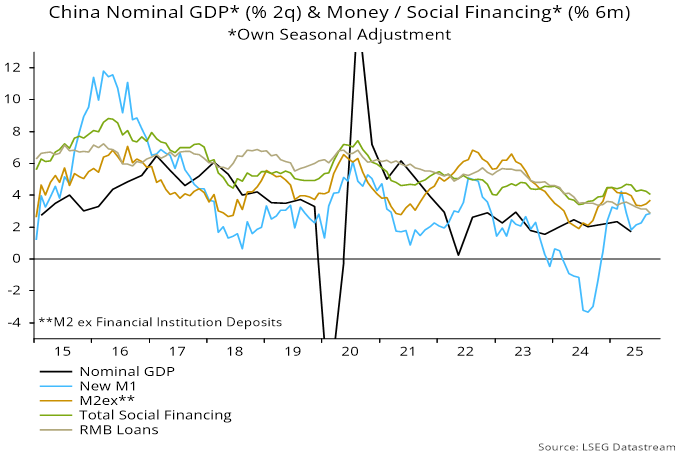

Six-month growth of narrow money – as measured by the new M1 definition incorporating household demand deposits – rose slightly in September, extending a recovery from a May low. Broad money momentum also edged higher. Both series are around their average levels in recent years – see chart 1.

Chart 1

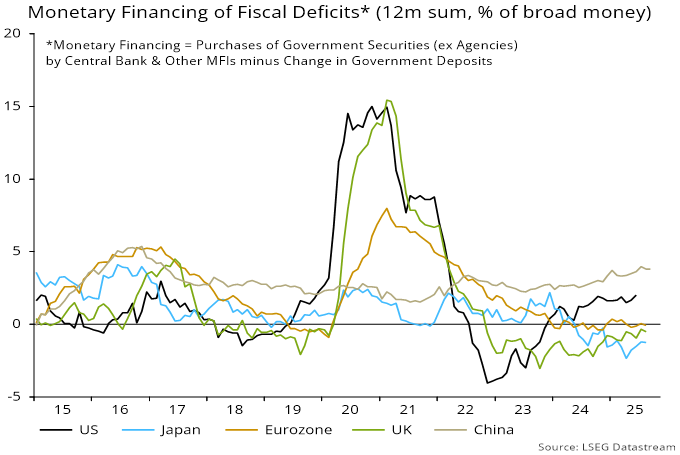

Credit trends remain weak, with six-month growth of bank lending reaching another record low, although numbers have been suppressed by bond swaps. Monetary expansion, however, continues to be boosted by China’s version of QE, conducted via the state banks. Monetary financing of the government, including bond swaps, accounted for 3.8 pp of M2 growth of 8.4% in the year to September – chart 2.

Chart 2

Money growth remains above nominal GDP expansion, arguing against a debt deflation scenario and suggesting “excess” money support for asset prices. With the housing market still weak and longer-term bond yields recently moving up from record lows, equities could remain the default beneficiary.