Chinese money update: slow recovery

Chinese money trends are normalising after weakness, suggesting modest economic improvement.

A previous post argued that a recovery in money growth was under way but the extent of reacceleration was uncertain. A revival remains on track but has so far proved lacklustre.

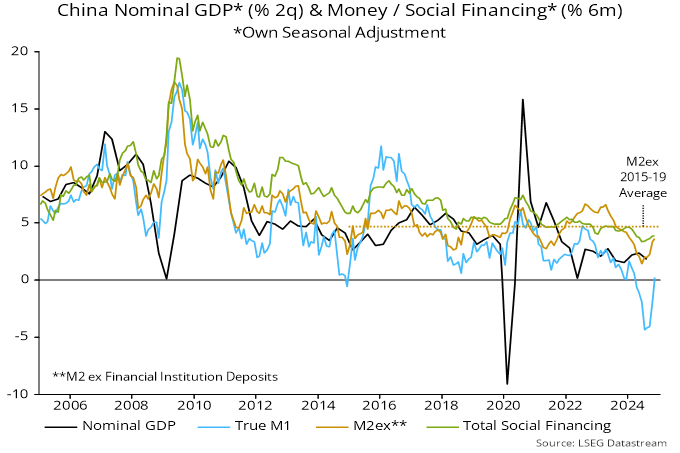

Money numbers were distorted in the spring by regulatory enforcement of deposit rate ceilings, which led to corporations switching out of demand deposits into time deposits and non-monetary instruments. Broader money measures were less affected, resulting in a focus here on the “M2ex” aggregate (i.e. official M2 minus deposits of financial institutions, which are volatile and less correlated with future activity / prices).

Six-month M2ex momentum bottomed in June and recovered further in November, though remains below its 2015-19 average – see chart 1.

Chart 1

Narrow money momentum is much weaker but has started to normalise as the spring distortion drops out of the six-month comparison. (The “true M1” measure shown approximates to a new official M1 definition to be adopted from January.)

Chinese money momentum has led nominal GDP momentum by two quarters on average historically, so monetary reacceleration since mid-year suggests better economic data from early 2025.

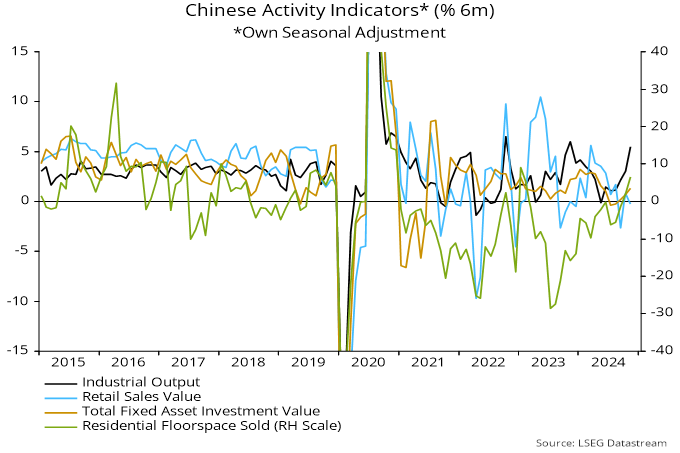

November activity numbers were positive on balance. Six-month rates of change of industrial output, fixed asset investment and home sales rose further but retail sales disappointed – chart 2. Output strength could reflect front-loading ahead of tariffs.

Chart 2

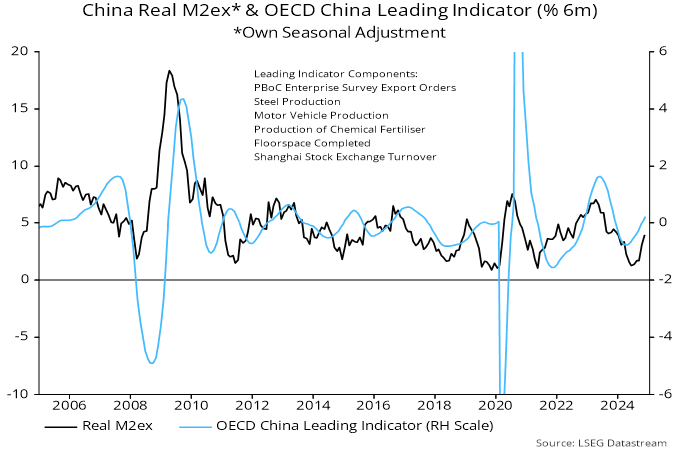

The suggestion from monetary trends of improving prospects is supported by the OECD’s composite leading indicator, six-month momentum of which has turned positive, suggesting above-trend growth – chart 3.

Chart 3

Real money momentum has led leading indicator momentum by four months on average historically but the low in the latter occurred earlier on this occasion, perhaps reflecting the regulatory distortion to monetary data mentioned above.