Are US monetary conditions about to tighten?

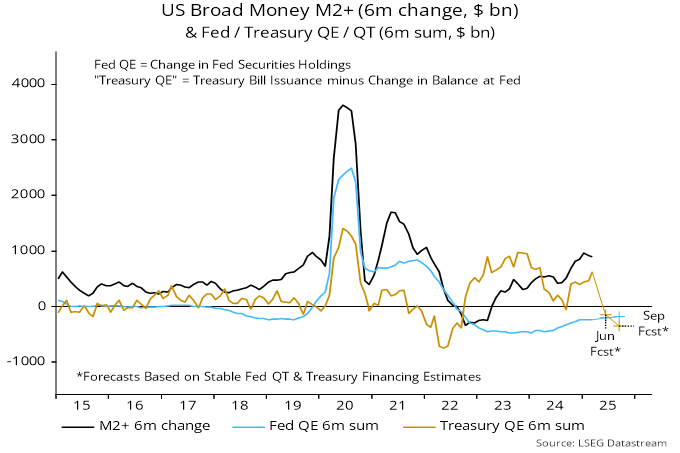

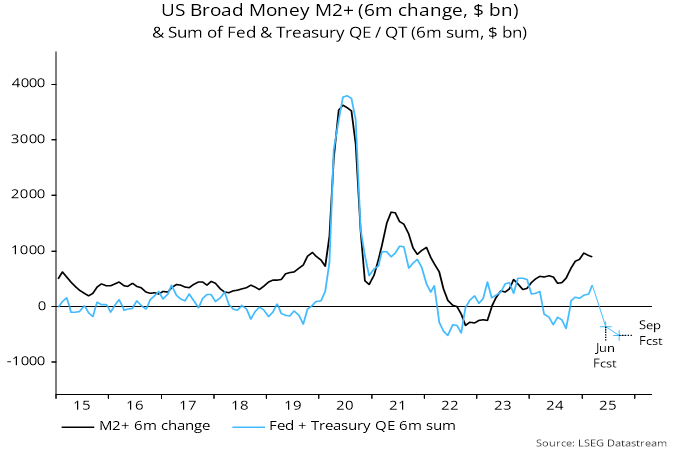

US broad – and probably narrow – money growth has been boosted recently by reduced issuance of Treasuries due to the debt ceiling constraint. The accompanying enforced run-down of the Treasury’s cash balance at the Fed has resulted in a resurgence of “Treasury QE”, a proxy for monetary deficit financing. This has more than offset (reduced) Fed QT – see charts 1 and 2.

Chart 1

Chart 2

Conditional on an early lifting of the debt ceiling, however, the Treasury’s financing estimates imply a dramatic reversal over the remainder of Q2 / Q3. The plans involve “catch-up” issuance to restore the Treasury balance to its prior level, with coupon debt – rather than bills – bearing most of the burden. (Coupon sales to non-banks contract the broad money stock; bills are more likely to be purchased by money funds and banks, implying a neutral monetary influence.)

The Fed could neutralise most of the negative Treasury impact by suspending QT. Still, the joint Fed / Treasury influence would swing from being significantly expansionary to neutral or slightly contractionary.

The suggested loss of money momentum could be offset by other factors. A similar swing in the joint influence in Q2 / Q3 2024 was associated with a minor slowdown in broad money as it coincided with a pick-up in bank lending growth.

Will a rebound in issuance put upward pressure on Treasury yields? Over 2010-19, Fed QE / QT – and the joint Fed / Treasury influence – was positively correlated (weakly) with the 10-year yield, i.e. the yield tended to rise when the Fed absorbed more supply and fall when it wound down purchases or ran down holdings.

A possible explanation is that the impact of the Fed’s actions on monetary trends and thereby economic prospects outweighed the direct yield impact of reduced or increased Treasury supply to the market. The suggested negative swing in the joint Fed / Treasury influence, therefore, could be associated with lower not higher yields.