Are Eurozone money trends inflecting weaker?

Eurozone March money numbers were mixed, suggesting that further ECB policy easing will be required to insulate the economy from global weakness.

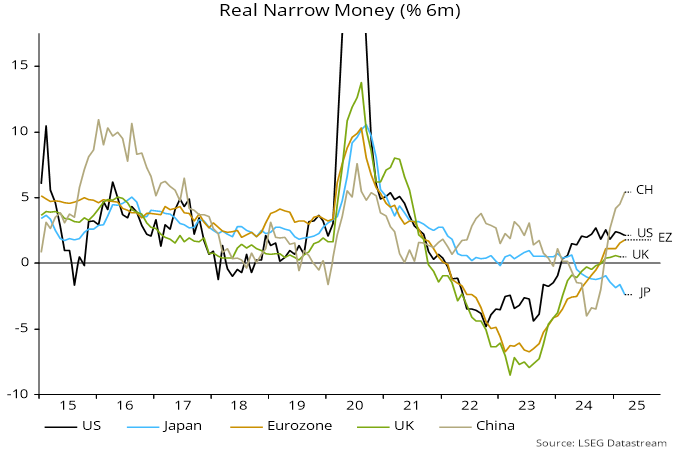

Positively, six-month real narrow money momentum rose further in March, almost closing the gap with the US – chart 1.

Chart 1

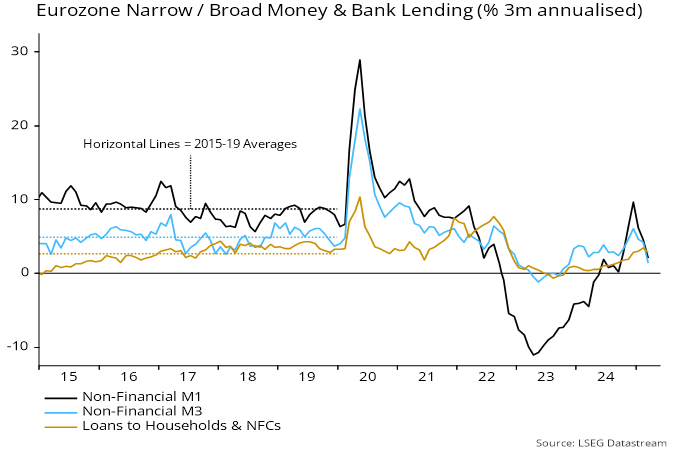

The six-month change, however, conceals a pull-back in growth in the latest three months, with broad money also slowing. Bank loan expansion has retained momentum but is a coincident / lagging indicator, while money leads – chart 2.

Chart 2

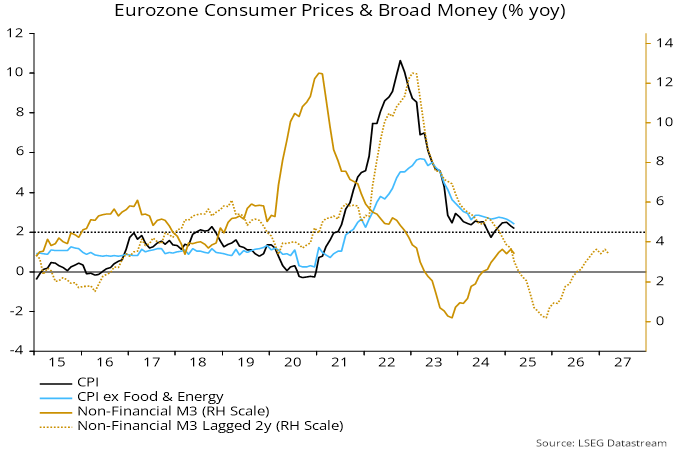

Annual broad money growth has stalled well below a level likely to be consistent with achievement of the 2% inflation target over the medium term – chart 3.

Chart 3

Weaker narrow money growth in the latest three months may reflect a downward revision of spending intentions in response to US policy news. A Q1 rise in longer-term bond yields may also have acted as a dampener, though has since reversed.

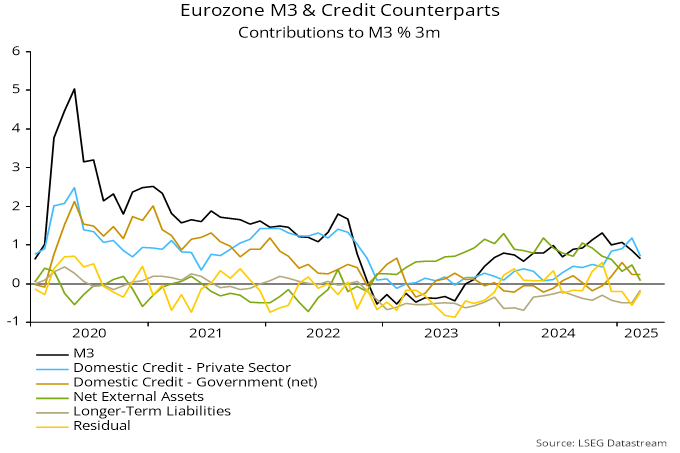

The fall in broad money growth was driven mainly by a slowdown in banks’ net external assets, according to the credit counterparts analysis. The government contribution has been positive recently, with the ECB’s passive QT more than offset by securities purchases by banks – chart 4.

Chart 4

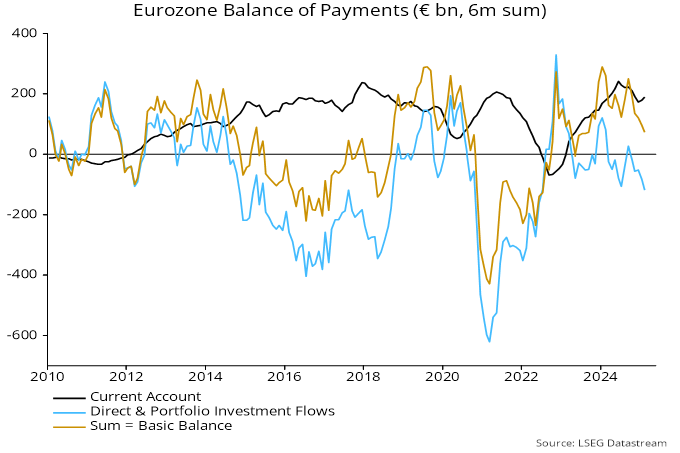

Conceptually, the change in banks’ net external assets is the counterpart of the basic balance of payments position (current account plus net direct and portfolio investment). The basic balance surplus has fallen back as the current account surplus has moderated and a deficit on the direct / portfolio capital account has widened – chart 5.

Chart 5

The capital account deterioration mainly reflects transactions in short-term debt securities, possibly motivated by changes in interest rate differentials.

Changes in the basic balance have been weakly correlated with exchange rate movements historically. Still, the fall in the surplus casts doubt on forecasts of further euro strength.